Analysis of Private Digital Currency Regulation in China

Analysis of Private Digital Currency Regulation in China

With the widespread adoption of blockchain technology, private digital currencies such as Bitcoin and Ethereum have garnered increasing attention. As a emerging financial instrument, private digital currency exhibits characteristics distinct from traditional legal tender, posing significant regulatory challenges for financial authorities. This article examines the regulatory framework for private digital currencies in China, analyzes existing regulatory gaps, and proposes policy recommendations.

I. Introduction

Private digital currencies, represented by Bitcoin, are decentralized digital currencies based on cryptographic principles and distributed ledger technology. Unlike traditional legal tender issued by central banks, private digital currencies operate through peer-to-peer networks without centralized issuing authorities. Since the inception of Bitcoin in 2009, the private digital currency market has experienced rapid growth, with total market capitalization reaching hundreds of billions of dollars. However, the anonymous, cross-border, and decentralized characteristics of private digital currencies have also provided opportunities for illegal activities such as money laundering and terrorist financing.

II. Current Regulatory Framework in China

A. Prohibition of Token Issuance and Financing

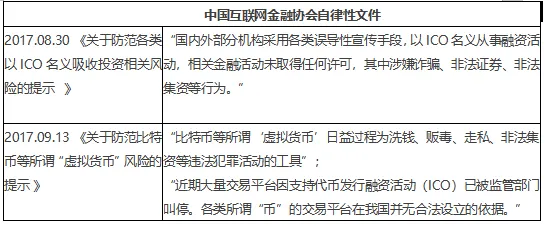

In September 2017, seven ministries and commissions including the People’s Bank of China jointly issued the Notice on Preventing Financial Risks from Token Issuance and Financing, clearly prohibiting legal persons, unincorporated organizations, and individuals from illegally raising funds through token issuance and financing activities. All token issuance and financing activities carried out in China are illegal and have been strictly prohibited.

B. Exchange Prohibitions

The notice also requires that domestic exchange platforms for token trading shall not engage in exchange services for tokens or provide pricing, intermediary, or trading services for tokens. Any exchange platforms established overseas that provide such services to domestic residents through the internet are also strictly prohibited.

C. Digital Currency Regulation

In 2021, the State Council issued the Notice on Strictly Preventing Financial Risks from Trading Cryptocurrencies, emphasizing once again that Bitcoin, Ethereum, and other private digital currencies are not legal tender and shall not circulate or be used in the market. Financial institutions, payment institutions, and internet platform enterprises shall not engage in any business activities related to private digital currency, including exchanging legal tender for private digital currencies or tokens, exchanging private digital currencies for tokens, trading or trading on behalf of others, providing storage or management services for private digital currencies, and issuing financial products related to private digital currencies.

III. Analysis of Regulatory Challenges

A. Cross-Border Transaction Challenges

The decentralized nature of private digital currencies enables transactions to bypass traditional financial systems, creating significant challenges for regulatory authorities. Cross-border transactions can circumvent foreign exchange controls and capital account regulations.

B. Anonymous Transaction Challenges

Private digital currencies utilize pseudonymous addresses, making it difficult to identify true transaction parties. This characteristic poses challenges for anti-money laundering and know-your-customer regulatory efforts.

C. Technical Complexity Challenges

The underlying technologies of private digital currencies, including blockchain and cryptographic techniques, require regulators to possess specialized technical knowledge and capabilities.

IV. Policy Recommendations

A. Strengthening International Cooperation

Regulatory coordination among countries should be enhanced to establish an international regulatory framework for private digital currencies.

B. Improving Technical Capabilities

Regulatory authorities should strengthen technical training and invest in supervisory technology (RegTech) to enhance monitoring capabilities for private digital currency transactions.

C. Clarifying Legal Attributes

The legal attributes of private digital currencies should be clarified through legislation to provide a foundation for regulation.

D. Promoting Blockchain Innovation

While strengthening regulation, appropriate space should be preserved for the development of legitimate blockchain technology applications.

V. Conclusion

The regulation of private digital currencies in China is complex and challenging. While strict prohibition protects financial stability, it also necessitates attention to technological innovation and development. Future regulatory efforts should seek to balance financial stability with technological innovation.