Practical Application of Insurance Trusts in Wealth Inheritance for High-Net-Worth Individuals

Practical Application of Insurance Trusts in Wealth Inheritance for High-Net-Worth Individuals

Attorney LI Dingbang systematically explores the application of insurance trust in wealth management. It first introduces the development background, establishment threshold, and regulatory status of insurance trusts, comparatively analyzing domestic Models 1.0 to 3.0 and operational mechanisms in the US, Japan, and Taiwan. Second, it elaborates on the core advantages of this instrument in tax planning, asset segregation from creditors, professional asset management, and flexible distribution. Then, drawing on practical cases, it identifies existing legal gaps in preventing beneficiary moral hazard, arrangements for the settlor's incapacity or incompetence, and post-mortem estate management, proposing comprehensive planning through supporting legal tools such as agreed guardianship and notarized wills. Finally, it emphasizes that the commercial optimization of insurance trusts requires cross-industry collaboration, and lawyers should play a key role in legal structure design and personalized wealth inheritance planning.

The Author’s Note: As one of the most popular financial products in the current wealth management and inheritance market, insurance trusts inherently contain complex and variable legal risks and issues. Drawing on recent practical cases of assisting clients in establishing insurance trusts, the author explores how lawyers can engage in insurance trust matters and integrate insurance trusts into the overall legal planning of wealth inheritance for high-net-worth individuals, from the perspectives of background, models and comparisons, advantages, and practical case planning, for the reference of colleagues.

I. Background

In 2023, with the successful claim settlement of Taikang Insurance’s first insurance trust case, this insurance product has become increasingly known. An insurance trust refers to a trust plan where, after the policyholder signs an insurance contract with an insurance company, the life insurance policy is used as trust property. The policyholder then signs a trust contract with a trust company cooperating with the insurance company, stipulating that the insurance proceeds payable at maturity are directly deposited into the trust account. The trust company manages and operates the insurance proceeds and distributes the trust property and income generated from managing the account to the trust beneficiaries in accordance with the trust contract. The current establishment threshold for insurance trusts is RMB 1 million in insurance premiums or insurance proceeds. This relatively low threshold has made it one of the hottest financial products in the current wealth management and inheritance market. After discussions with industry insiders, the author learned that Bank of China三星 Life Insurance has even developed a living insurance trust product, which to some extent changes the traditional definition of “insurance trust,” demonstrating how huge market demand drives the iteration of financial products.

According to the “2024 China Private Wealth Report” jointly released by China Merchants Bank and Bain & Company, the number of high-net-worth individuals in China reached 3.66 million in 2024, holding RMB 121 trillion in investable assets, with a compound annual growth rate of 7% from 2020 to 2024. The accumulation and growth of wealth have given rise to the demand for wealth management among the high-net-worth群体. As a new tool combining insurance and trust to achieve asset management and wealth inheritance, insurance trusts have attracted significant attention. However, research on insurance trusts is currently limited, and the supporting regulatory system and norms are not yet健全. From the first落地 case in 2014 until 2023, when the former China Banking and Insurance Regulatory Commission issued the “Notice on Regulating the Classification of Trust Business by Trust Companies,” classifying insurance trusts as asset service trusts under wealth management service trusts, insurance trusts finally received formal regulatory recognition after nearly a decade of尴尬 cross-industry regulatory ambiguity.

II. Analysis and Comparison of Existing Models

(I) Domestic Existing Models

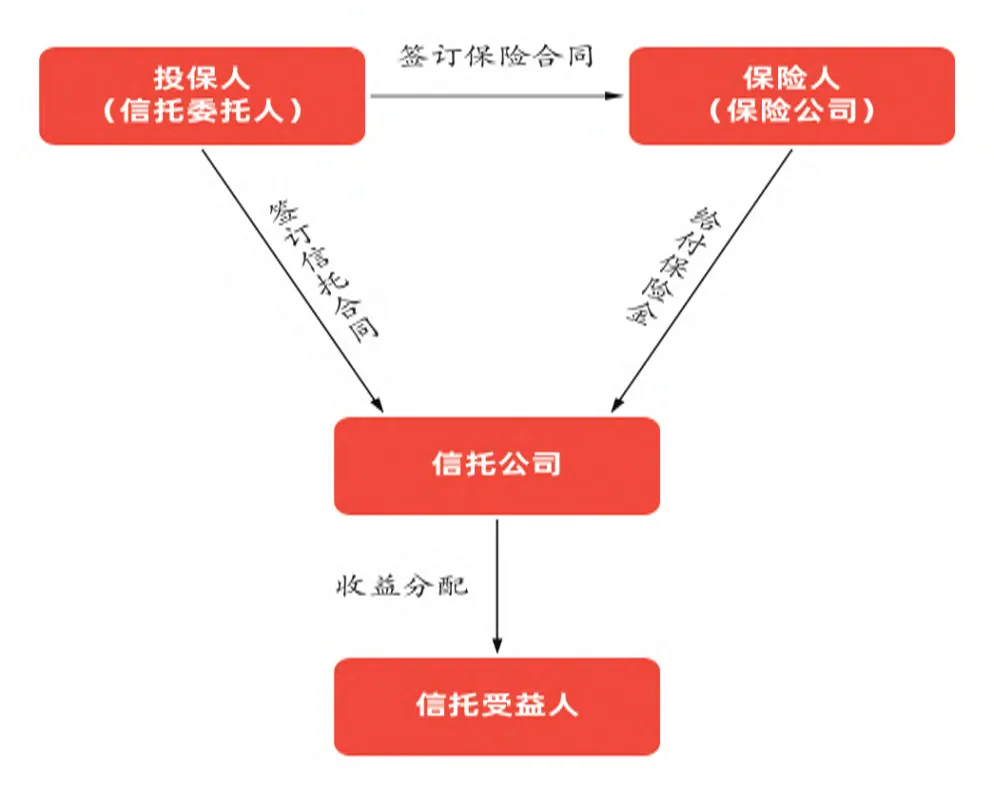

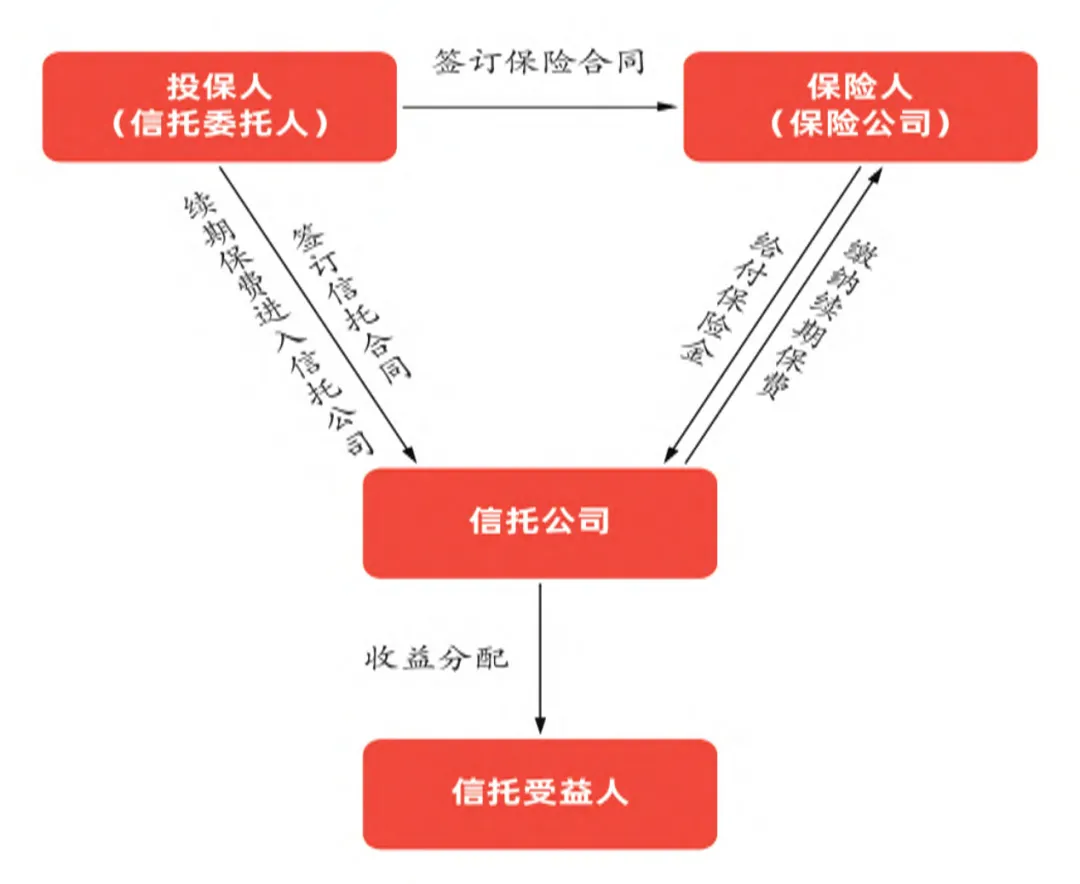

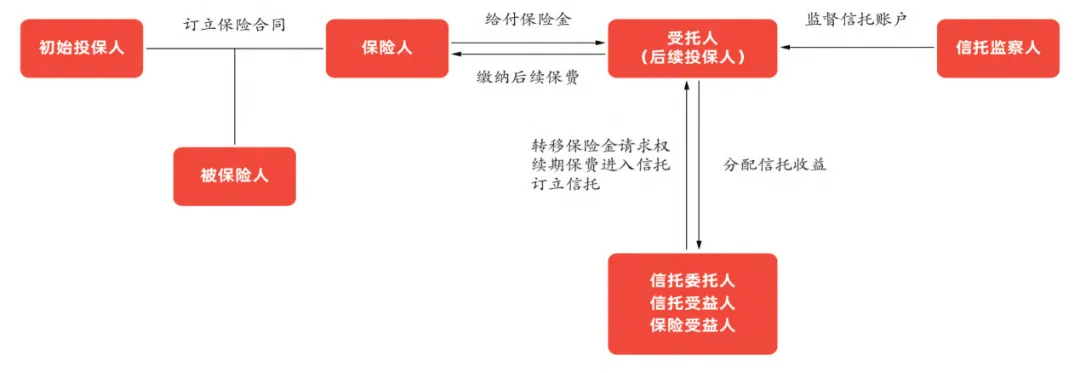

Currently, three mainstream operational models exist in the insurance trust business: Insurance Trust 1.0, 2.0, and 3.0. The traditional 1.0 model involves the settlor taking out insurance independently, using the policy benefit rights or insurance proceeds as trust property to establish an insurance trust. With the consent of the insured, the insurance beneficiary is changed to the trust company. Upon the occurrence of an insured event, the insurance proceeds are paid by the insurance company to the trust company, which, as the trustee, manages and disposes of the trust property in accordance with the trust document. In the 2.0 model, after establishing the insurance trust with the insurance product, the settlor needs to change both the policyholder and the insurance beneficiary to the trust company, with the trust company using the trust property to pay subsequent premiums. The 3.0 model follows a “trust first, insurance later” approach, where the settlor establishes a trust with their own property, and the trust company uses the trust property to purchase insurance products and pay premiums.

1.0 Model

2.0 Model

3.0 is similar in logic to 2.0, with the only difference being the order of the first two steps.

First, establish a family trust, place premiums as trust property into the trust, then purchase insurance policies and act as beneficiary in the name of the trust.

(II) Comparative Systems

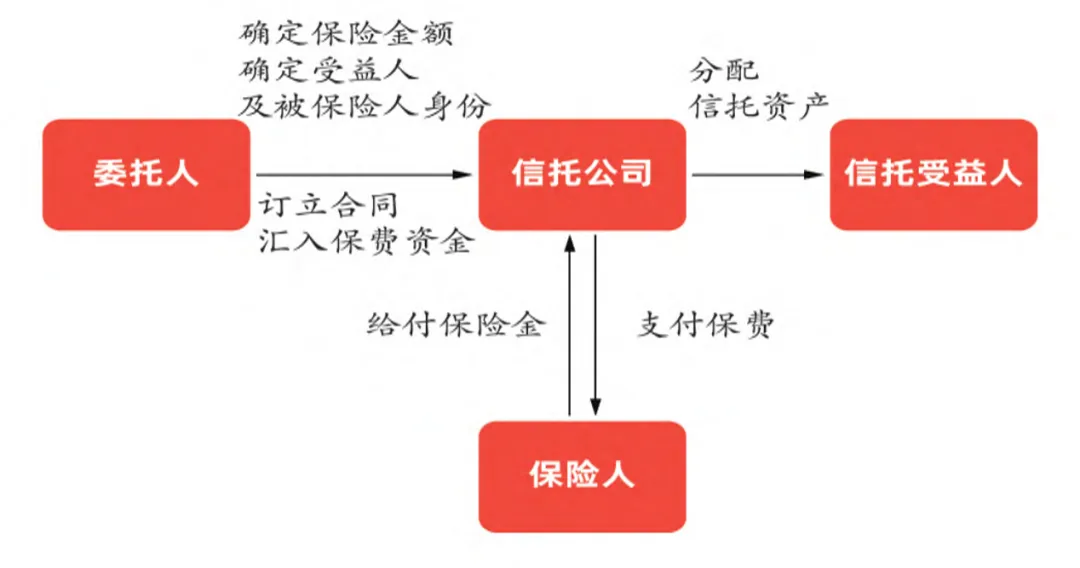

In the United States, there are two operational models for irrevocable life insurance trusts. The first involves the settlor using the ownership of the insurance policy as the trust property to establish an insurance trust. The settlor first enters into an insurance contract with the insurance company, then transfers the effective policy as trust property into the trust account. The settlor transfers ownership of the effective policy to the trust company, which, after obtaining policy ownership and written consent from the insured, changes itself to the new policy beneficiary. The second involves the settlor using a portion of property and a life insurance policy as trust property to establish an insurance trust. The settlor first enters into a trust contract with the trust company and deposits some funds into the trust account, entrusting the trust company to purchase life insurance on their behalf. Both models require policy ownership to be held by the trust company, so that when an insured event occurs, the insurance proceeds paid by the insurance company enter the trust company’s trust account. The operational model is illustrated below.

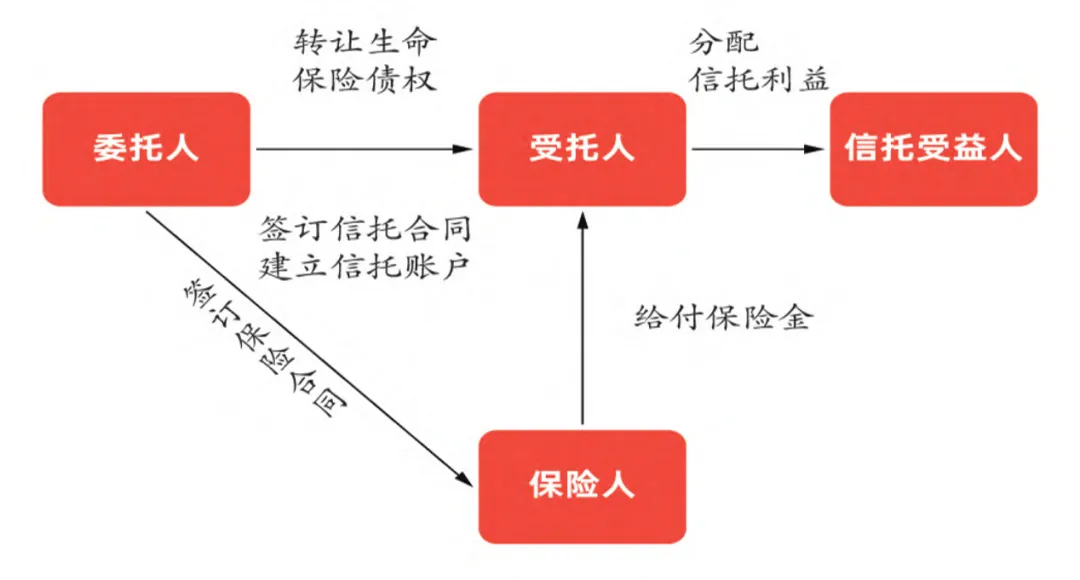

In Japan, life insurance is commonly referred to as “生命保険” (life insurance), so trusts established with life insurance proceeds are also called “生命保険信託” (life insurance trust). In Japan’s “life insurance trust,” the settlor assigns the claim for life insurance proceeds to the trustee. The trust settlor is also the insurance policyholder and insurance beneficiary, and the trustee is the trust company. After the policyholder enters into the insurance contract with the insurance company, upon maturity or the occurrence of an insured event, the trustee receives the insurance proceeds and manages, operates them or delivers them to the beneficiary in accordance with the trust contract. The operational model is illustrated below.

In the Taiwan region of China, the current insurance trust model is divided into two types based on the relationship between beneficiary and settlor: altruistic insurance trusts and self-benefiting insurance trusts. In an altruistic insurance trust, the trust settlor and beneficiary are not the same person. The most common form is where parents are the insured and trust settlors, while children are the insurance beneficiaries and trust beneficiaries. In a self-benefiting insurance trust, the trust settlor and beneficiary are the same person, typically where a child simultaneously holds the triple identity of insurance beneficiary, trust settlor, and trust beneficiary. When the policy triggers a payment or upon maturity, the insurance proceeds are deposited into the trust account. The business model is illustrated below.

III. Advantages of Insurance Trusts

Generally speaking, insurance trusts not only have the front-end insurance functions, particularly for large life insurance policies, such as designated beneficiaries, leverage, and savings, but also possess the back-end trust attributes, such as property independence, conditional or installment payments. Specifically, their advantages include:

(I) Legal Tax Planning (Not yet available in Mainland China)

The rapid growth of irrevocable life insurance trusts in the United States into a massive financial business is closely linked to their tax planning function. As is well known, the United States is a typical country that imposes estate tax. U.S. tax residents, such as U.S. citizens and green card holders, are subject to estate tax on their worldwide assets. Pursuant to Section 2042 of the U.S. Internal Revenue Code, for life insurance policies insuring a U.S. person, the insurance proceeds are included in the insured’s estate in two scenarios: first, if the insured’s estate executor receives the life insurance proceeds upon the insured’s death; second, if the insurance proceeds are paid to someone else, but the insured retained “incidents of ownership” in the policy before death. To legally avoid taxation, the insurance trust (ILIT) emerged. Since the ILIT is an irrevocable trust, once the settlor transfers property into the irrevocable trust, the ownership of the property substantively transfers and is no longer part of the settlor’s controllable personal property. Therefore, the insurance proceeds are no longer included in their estate. Besides avoiding estate tax, the ILIT can also effectively utilize the annual gift tax exclusion, exerting significant leverage. However, the trustee must send “Crummey Notices” to all beneficiaries after the settlor contributes cash assets, informing beneficiaries of their “withdrawal rights.” It should be noted that China currently does not have estate tax or generation-skipping transfer tax. However, considering that insurance trusts are part of family inheritance and have a duration of 30-50 years or even over a century, it is possible that estate tax and other laws may be enacted during this period. Therefore, the tax planning function of insurance trusts remains relevant.

Thus, the tax planning function of insurance trusts should not be absolutized, nor should it be promoted as a major selling point. It must be considered comprehensively based on the actual circumstances at the time. For example, the Ministry of Finance of Taiwan issued an interpretive letter on January 18, 2013, providing examples and reference characteristics for assessing estate tax on death life insurance proceeds under the principle of substantive taxation. These can be summarized into eight patterns: (1) purchasing insurance during serious illness; (2) lump-sum premium payment; (3) purchasing insurance with borrowed funds; (4) purchasing insurance at an advanced age; (5) short-term insurance; (6) large-sum insurance; (7)密集 insurance purchases; (8) insurance benefits lower than or equivalent to paid premiums plus interest. In such cases, tax authorities can determine the severity of “malicious insurance purchase” based on the policyholder’s actual circumstances for look-through taxation. Once Mainland China establishes estate/gift taxes in the future, relevant laws and regulations such as the “Tax Collection and Administration Law” and “Individual Income Tax Law” are also expected to regulate “malicious insurance purchase” behavior, further specifying the application of general anti-avoidance rules.

(II) Blocking Creditors’ Pursuit of Policy Cash Value (Especially Insurance Trust 2.0 and 3.0 Models)

Life insurance policies, especially whole life insurance, generally have high cash value. The cash value of a policy is the value inherent in a long-term personal insurance contract, typically reflected as the amount the insurance company returns to the policyholder upon surrender. The cash value of a policy is generally owned by the policy owner. If the policy owner becomes insolvent, their creditors may sue in court to use the cash value to satisfy debts. To address this, the policy can be placed in a trust (usually an irrevocable trust), or the trust can take out the insurance. Once the policy is placed in the trust, the policy owner changes from the individual to the trust itself, and creditors of the original policy owner can no longer demand that this asset be used to repay debts. It can be seen that insurance trusts can effectively protect the cash value of the policy from being pursued by the policy owner’s creditors. However, like general trusts, the risk insulation of insurance trusts must meet specific conditions, including that the settlor was not insolvent at the time of trust creation, the trust was not established to maliciously evade debts, and the creditor’s claim arose after the trust was established.

(III) Professional Asset Management and Flexible Benefit Distribution

Insurance trusts combine the respective advantages of insurance and trusts. Compared to rigid policy payout mechanisms, especially the一次性 payment of large insurance proceeds to beneficiaries who lack professional management capabilities, the asset management and flexible distribution advantages of insurance trusts are very prominent. On the one hand, the trustee of an insurance trust can centrally manage multiple policies with different rules from different insurance companies, distribute according to a unified plan, and provide assistance when beneficiaries truly need it. The trustee can also, in accordance with the prudent investor rule, monitor the financial condition of insurance companies in real-time and adopt certain portfolio investment measures. On the other hand, after the insured’s death, the trustee will make flexible distributions to beneficiaries such as family members according to the distribution frequency, time, conditions, and objectives set by the settlor in the trust contract. When, where, how, and why beneficiaries receive insurance proceeds are strictly controlled by the settlor’s intent. This not only fully protects the family’s livelihood and guides their growth but also prevents insurance proceeds from being squandered or pursued by beneficiaries’ creditors, achieving the settlor’s planning goals. Furthermore, to increase the flexibility of the insurance trust, an independent third party can be appointed as trust protector, who can modify the trust document, change beneficiaries, or adjust trust distribution terms based on the trust’s operation and changes in circumstances.

IV. Legal Issues with Insurance Trusts

Although insurance trusts have unparalleled advantages and development prospects, practical issues were discovered in the actual cases the author participated in.

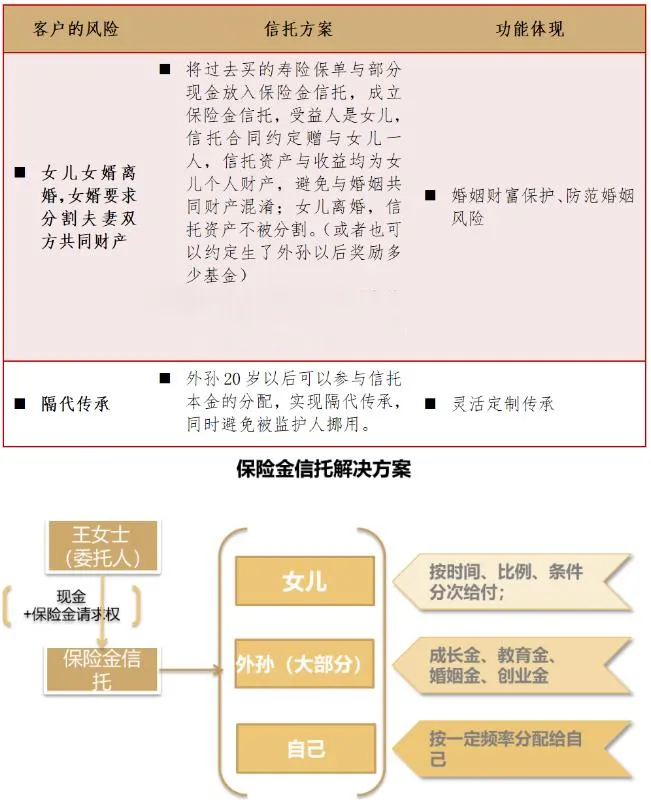

Case background: Ms. Wang, a renowned calligrapher in Changsha, Hunan, has four children. She was widowed early and has never remarried. Her four children live abroad permanently and have established their own families. Ms. Wang hires a full-time caregiver. She owns real estate, vehicles, artworks, antiques, financial assets, and bank deposits totaling RMB 240 million. Considering her advanced age and an 85% probability of developing Parkinson’s disease within the next three years, she needs to make special arrangements for herself and her children while still lucid, to maintain her dignity in old age and ensure harmony among her children. Her eldest daughter faces the risk of divorce; she adores her young grandson but does not want to spoil him, wishing to provide financial support or encouragement when he needs it. Her youngest daughter has poor spending habits and unstable employment, causing Ms. Wang to worry about her future life and work.

Insurance trust setup: Ms. Wang had previously purchased a term life insurance product from a certain insurance company, with an expected death benefit of RMB 10 million. Due to product promotion needs, an insurance agent introduced her to a back-end trust, and she added RMB 1 million in cash deposits to the trust. This is the most popular insurance trust 1.0 model. The specific design plan for this case is illustrated below:

It can be seen that this insurance trust facilitated Ms. Wang’s asset preservation and inheritance. However, many issues remain, particularly its inability to independently address the dynamic problems during Ms. Wang’s subsequent mental and physical health stages:

First, Ms. Wang’s normal survival period. The daughters and grandson, as beneficiaries, pose potential moral hazard within the entire structure, but no legal rules address this. For inheritance or gifts, there are grounds for revocation if the heir or donee engages in conduct seriously harming the principal’s interests. Similar provisions exist in insurance law and trust law. However, when insurance and trust are combined in an insurance trust, there is a “regulatory gap” concerning the beneficiaries of the insurance trust, because strictly from a legal concept perspective, they cannot be subsumed under any single legal角色. Although some scholars advocate for analogous application of relevant rules to regulate the conduct of insurance trust beneficiaries, uncertainty exists in potential future disputes. Therefore, when serving this case, especially when the trust company was reluctant to modify the trust contract terms, we specifically had the insurance trust beneficiary sign a confirmation letter kept at the notary office, explicitly stating that if they engage in conduct harmful to Ms. Wang, fight for inheritance to the detriment of other beneficiaries, or fail to visit or abandon Ms. Wang, their right to insurance trust benefits is automatically forfeited.

Second, Ms. Wang’s potential incapacity or incompetence. Although Ms. Wang herself is a beneficiary of the insurance trust, the insurance trust structure alone cannot address how she would receive and use trust benefits if she becomes incapacitated or incompetent, leaving a gap in securing her晚年 life. We also suggested that Ms. Wang establish a separate special needs trust. However, given that the insurance trust was already established, potential conflicts between the two trusts, and the trust company’s service fees and willingness, Ms. Wang ultimately did not choose to establish a special needs trust. Therefore, we collaborated with the notary office to incorporate an agreed guardianship agreement into the trust agreement. This stipulates that when a hospital confirms Ms. Wang’s Parkinson’s diagnosis, the agreed guardian designated in the agreement begins to assist in exercising the rights and obligations pertaining to Ms. Wang as a beneficiary under the trust agreement. In this way, we can design more specialized content in the agreed guardianship agreement, such as medical services, care, and health maintenance, forming a complete framework with the insurance trust agreement.

Third, upon Ms. Wang’s death when insurance proceeds enter the trust. The agreed guardianship agreement currently only takes effect after Ms. Wang becomes incapacitated or incompetent. The insurance trust truly takes effect only after Ms. Wang’s death. However, we found that no entity can stand in a relatively neutral position to handle Ms. Wang’s estate matters. Insurance represents only a portion of Ms. Wang’s overall wealth, and this part needs to be integrated into a broader wealth inheritance plan. To fill this gap, we again collaborated with the notary office to assist Ms. Wang in drafting a notarized will, designating an estate administrator, and specifically defining the administrator’s rights and obligations, providing ongoing post-mortem supervision of Ms. Wang’s entire wealth (including insurance) and offering strong support from an external legal perspective for the operation of the insurance trust. Considering that many insurance companies and trust companies engaged in insurance trust business, based on cost and internal compliance considerations, are unwilling to allow the settlor to add a trust protector/supervisor, we needed to find alternative paths to achieve a secure package for wealth inheritance.

V. Conclusion

From the above, it can be seen that optimizing the business model of insurance trusts is a systematic project requiring joint efforts and innovative thinking from all parties within and outside the industry. By implementing effective optimization strategies, insurance companies and trust companies can not only enhance their own competitiveness but also provide customers with better and more personalized services, thereby maintaining a leading position in the ever-changing market environment. In the future, with technological progress and market development, the insurance trust industry is expected to achieve more diversified and intelligent development, creating greater value for customers and society.

The importance of lawyers in the insurance trust business is undeniable. From front-end design, mid-term maintenance, to back-end conflict resolution, deep involvement by lawyers is necessary. Unlike insurance companies, trust companies, and banks, we need to provide intellectual support for insurance trust business more from the perspective of legal architecture and rule operation, rather than simply treating it as a financial management tool or a hot product. We need to understand, behind the insurance trust, the specific parties in each particular social and family context, where there are their big or small expectations, demands, tears, and smiles that have nothing to do with the amount of wealth, and more importantly, the warmth and coldness of human nature behind the rule design. Can this insurance trust structure be warmer or crueler? Can it be ephemeral or continuously burst with vitality? These are profound questions that all lawyers engaged in the wealth management field need to冷静思考 and passionately serve! Let us all work together!