How to Determine the Guarantee Period When Its Stipulated Start Date Precedes the Maturity Date of the Principal Debt?

How to Determine the Guarantee Period When Its Stipulated Start Date Precedes the Maturity Date of the Principal Debt?

Regarding the validity of a clause stipulating the start of the guarantee period earlier than the date of maturity of the principal debt, this article, referencing Article 692 of the Civil Code, points out that although such a situation is generally deemed as no agreement in principle, in practice, the validity of the agreement should be determined based on the end date of the guarantee period: the provision on the start date is invalid because it violates the principle of accessory nature of guarantee and should be legally corrected to the date of maturity of the principal debt, while the agreement on the length of the period or the end date remains valid. Drawing on judicial cases and legal analysis, the article explores the typified application rules for such clauses, pointing out that an excessively short guarantee period may be deemed invalid for violating the principle of good faith, and offers practical suggestions that the start of the guarantee period should be stipulated on or after the date of maturity of the principal debt, and the length of the period should be moderate to avoid legal risks.

Recently, while reviewing a guarantee contract, the author encountered the following clause regarding the guarantee period: “Our guarantee period shall commence on the effective date of this Contract and end seven days after the date on which the project payment under the main contract is fully paid.” That is, the starting point of the guarantee period is stipulated as the effective date of the guarantee contract, which is earlier than the date of maturity of the principal debt, differing from the statutory starting point for the guarantee period. So, what is the validity of this clause? When the agreed starting point of the guarantee period is earlier than the maturity of the principal debt, how should the guarantee period be determined?

Article 692 of the Civil Code contains provisions on the guarantee period. Paragraph 2 of that article clarifies: “The creditor and the surety may agree on a guarantee period; however, if the agreed guarantee period expires earlier than or at the same time as the performance period of the principal debt, it shall be deemed as no agreement. If there is no agreement or the agreement is unclear, the guarantee period shall be six months from the date on which the performance period of the principal debt expires.”

Thus, regarding the above agreement on the guarantee period, two views exist. View One: Because the agreed starting point of the guarantee period is earlier than the performance period of the principal debt, it falls under the circumstance of “the agreed guarantee period expires earlier than the performance period of the principal debt” as stipulated in Article 692, paragraph 2 of the Civil Code, and therefore should be deemed as no agreement, resulting in the application of “the guarantee period shall be six months from the date on which the performance period of the principal debt expires.” View Two: The agreement on the starting point of the guarantee period (“the effective date of the guarantee contract”) is invalid, and the statutory rule for the starting point should apply, i.e., “the guarantee period shall be calculated from the date on which the performance period of the principal debt expires.” However, the agreement on the end date of the guarantee period should be valid. Both views agree on the starting point; the difference lies in the termination point. Regarding this issue, the author’s research and analysis are as follows:

I. The Guarantee Period is Determined by the Principle of “Agreement Priority, Statutory Supplementation,” but the Parties’ Agreement Must Not Contravene the General Principles of Guarantee

The guarantee period is the period agreed upon by the parties or prescribed by law during which the surety bears the guaranty debt. This period is a fixed period, not subject to suspension, interruption, or extension, and is governed by a mandatory principle. If the creditor does not act in the legally prescribed manner within the guarantee period, the surety is released from the guaranty liability upon expiration of the period. Therefore, the guarantee period is a system designed to protect the surety and urge the creditor to exercise their rights, enabling the prompt determination of guaranty liability. According to Article 692 of the Civil Code, the determination of the guarantee period follows the principle of “agreement priority, statutory supplementation.” The parties are free to agree on the guarantee period; statutory rules apply only when there is no agreement or the agreement is unclear.

Guarantee is accessory in nature, reflected in many aspects such as the creation, extinguishment, modification, scope of liability, defenses, and effects of the guaranty debt. Article 701 of the Civil Code provides: “The surety may assert the debtor’s defenses against the creditor. If the debtor waives their defenses, the surety still has the right to assert defenses against the creditor.” That is, if the starting point of the guarantee period is earlier than the maturity date of the principal debt, the surety may also assert the principal debtor’s defenses and not bear guaranty liability before the maturity date of the principal debt. Therefore, the parties’ agreement on the guarantee period should not contravene the general principles of the guarantee system. Stipulating a starting point for the guarantee period earlier than the maturity of the principal debt contradicts the accessory nature of the guarantee and is also impracticable.

II. Determining “Guarantee Period Expiring Earlier than or Simultaneously with the Principal Debt Performance Period” Should Be Based on the End Date of the Guarantee Period

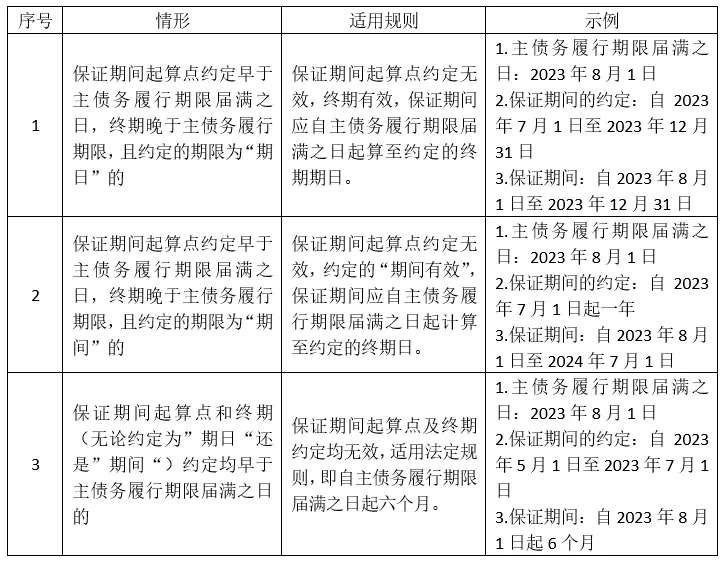

The guarantee period is a period of time, not a point in time. Determining the guarantee period involves two aspects: first, the starting point; second, the end point (or the length of the guarantee period). Where the performance period of the principal debt is ascertainable, three possible scenarios exist regarding the relationship between the parties’ agreement on the guarantee period and the maturity date of the principal debt:

1. Both the start and end of the agreed guarantee period are earlier than the maturity date of the principal debt;

2. Both the start and end of the agreed guarantee period are later than the maturity date of the principal debt;

3. The start of the agreed guarantee period is earlier than the maturity date of the principal debt, but the end date is later.

For Scenario 1, the rule “the agreed guarantee period expires earlier than or simultaneously with the performance period of the principal debt shall be deemed as no agreement” applies, leading to the statutory guarantee period. This is generally undisputed. For Scenario 2, the agreement does not violate mandatory legal provisions and should be lawful and valid. Delaying the starting point of the guarantee period can also strengthen the “subsidiarity” of the guaranty debt.

This article focuses on Scenario 3. The author believes that the determination of “the guarantee period expires earlier than or simultaneously with the performance period of the principal debt” should be based on the agreed end date of the guarantee period. In this scenario, the agreement on the starting point should be deemed invalid, the statutory starting point rule should apply, but the agreement on the end date of the guarantee period should be valid.

Therefore, the author agrees with View Two. View Two corrects the starting point to align with the general principles of the guarantee system, balancing respect for the parties’ autonomy with adherence to the fundamental rules of the guarantee period. The contracting parties may have agreed on “commencement from the effective date of this contract” due to insufficient understanding of the guarantee system. However, it is undeniable that the mutual agreement on the end date of the guarantee period is clear and consistent. Respecting the true intent of the parties also supports View Two.

Judicial practice supports this view. For example, the Shanxi Provincial High People’s Court in Case (2020) Jin Min Shen No. 820 held: “In this case, the reapplicant Duan, as surety, together with the respondent company and the third party Lei, signed a guaranteed loan contract. Article 11 stipulated ‘from the effective date of this contract until two years after the date on which the debt performance period under this contract expires.’ Judging from the content, it mainly stipulated the guarantee period for the loan in question. Although the agreed starting time of the guarantee period was earlier than the principal debt performance period, it also stipulated an end date of two years after the debt performance period expired. The expression clearly defined the guarantee period and did not fall under the circumstances that should be ‘deemed as no agreement’ or ‘deemed as unclear agreement.’” The Henan Province Yuzhou City People’s Court in Case (2012) Yu Min Yi Chu Zi No. 934 held: “The loan contract stipulated that the guarantee period was from the date of borrowing to two years after the loan’s maturity. The defendant Wang, as a joint and several liability surety, had an agreed guarantee period starting earlier than the principal debt performance period, which does not comply with legal provisions. Considering the agreement in the loan contract (the guarantee period was from the date of borrowing to two years after the loan’s maturity), the guarantee period for this loan should be determined by law as starting from the date of maturity of the principal debt, i.e., September 24, 2011, and lasting two years until September 24, 2013.”

III. Typification and Rule Application of “Guarantee Period Starting Earlier than Principal Debt Maturity Date”

Where the principal debt performance period is clear, several different scenarios exist for “the agreed starting point of the guarantee period being earlier than the maturity date of the principal debt.” It is necessary to conduct a typified analysis.

It should be noted that for Scenario 2 above (where the period is agreed as a “duration”), although the starting point of the guarantee period should be calculated from the date of maturity of the principal debt, the end date should not be determined as the maturity date of the principal debt plus the agreed duration. That is, the end date of this guarantee period is not August 1, 2024 (one year from August 1, 2023). Therefore, although a certain duration rather than a specific date is agreed, if a specific date can be determined from the content of the agreement, the true intent of the parties should be respected and their reasonable expectations protected.

IV. Extended Analysis and Suggestions on Stipulating the Guarantee Period

1

Is a Seven-Day Guarantee Period Too Short?

Returning to the contract clause we analyzed, based on a correct understanding of the guarantee period and exploring the true intent of the parties, the actual guarantee period in this situation should be seven days from the date of maturity of the principal debt. This raises a question: is a seven-day guarantee period too short and unfair to the creditor?

A guarantee period shorter than the statutory guarantee period is termed a “short-term guarantee.” The length of the guarantee period is a matter for the parties to agree upon freely. A short-term guarantee, being the parties’ mutual agreement, should be valid. However, some argue that the agreed length of the guarantee period should not violate the principles of good faith and public order and good customs. If the agreed guarantee period is so short that it makes it extremely difficult or impossible for the creditor to assert the guaranty claim, it should be deemed as no agreement, and the statutory guarantee period should apply.

In the Xiaoshan District People’s Court Case (2012) Hang Xiao Shang Chu Zi No. 3138, the court held: “The so-called guarantee period refers to the period during which the surety bears guaranty liability for the principal debt whose performance period has expired, as stipulated by law or agreed in the guarantee contract. According to relevant provisions of the Security Law, the guarantee period is divided into ‘agreed’ and ‘statutory’ situations. If the agreed guarantee period is shorter than six months, in principle, the agreement should prevail, but subject to not violating the principles of good faith and public order and good customs. In this case, the principal debt matured on February 17, 2012. The guarantee period recorded by Tong in the guarantee document ended on February 18, 2012, making the actual guarantee period only one day. Considering that Tong and Weng were friends, the loan from Qian was introduced by Tong, and the guarantee document was drafted by Tong, the court found that a one-day guarantee period promised by Tong was too short. This agreement excessively restricted the creditor’s ability to exercise the guaranty claim, violated the principle of good faith and common sense, and made it very difficult for the creditor Weng to assert the guaranty claim, which was extremely unfair to him. Therefore, the agreement was deemed as no agreement, and the statutory guarantee period applied. Since Weng’s claim against Tong for the guaranty had not exceeded the six-month statutory guarantee period, the court determined that Tong’s guaranty liability had not been discharged and he should still bear corresponding guaranty liability within the agreed scope.”

2

Suggestions on How to Stipulate the Guarantee Period

First, regarding the agreement on the starting point of the guarantee period. Based on the above analysis, where the principal debt performance period is ascertainable, stipulating the starting point of the guarantee period earlier than the maturity date of the principal debt may lead to the application of different rules. Subtle differences in the parties’ agreement can result in significant differences in the applicable rules and legal effects. Real-world situations are more complex. If the contract does not clearly specify the principal debt performance period or disputes arise concerning it, the uncertainty regarding whether the surety should bear guaranty liability increases. Therefore, to reduce disputes and maintain reasonable expectations, the starting point of the guarantee period should be stipulated as the date of maturity of the principal debt or thereafter.

Second, the agreed length of the guarantee period should be moderate. Generally, a short-term guarantee is more favorable to the surety. However, if an excessively short period is agreed upon, making it objectively impossible for the creditor to assert their claim, the court may deem it as “violating the principle of good faith, deemed as no agreement,” and apply the 6-month statutory period. Compared with agreeing on a 4-month or 6-month guarantee period, agreeing on an excessively short period may actually be disadvantageous to the surety. Conversely, agreeing on a longer guarantee period is generally favorable to the creditor. However, there is a risk that the creditor may become lax in exercising their rights due to the longer guarantee period, causing the statute of limitations against the principal debtor to expire. The surety may then assert the principal debtor’s statute of limitations defense and avoid bearing guaranty liability, even if the guarantee period has not yet expired.