Analysis of Cross-Border E-commerce Foreign Exchange Compliance: Lessons from Shanghai Bank's 100 Million Yuan Fine

Analysis of Cross-Border E-commerce Foreign Exchange Compliance: Lessons from Shanghai Bank's 100 Million Yuan Fine

Recently, the Shanghai Branch of the State Administration of Foreign Exchange published an administrative penalty decision against a Shanghai bank, imposing a warning and fines of nearly 100 million yuan for violations in foreign exchange transactions including spot exchange, foreign currency wealth management, and guarantee-backed lending. This article examines compliance issues in cross-border e-commerce foreign exchange transactions.

I. Background

Recently, the Shanghai Branch of the State Administration of Foreign Exchange published an administrative penalty decision against a Shanghai bank, imposing a warning and fines of nearly 100 million yuan for various foreign exchange violations including spot exchange, foreign currency wealth management, internal-guarantee external lending, and foreign exchange market transactions. While the penalized entity was a banking institution, this enforcement action has direct implications for cross-border e-commerce exporters.

In the cross-border e-commerce sector, particularly in retail export, due to the large volume and dispersed nature of exported goods, cross-border merchants face challenges when applying for exchange settlement through domestic banks via third-party payment institutions. Traditional methods for verifying transaction authenticity become difficult to implement.

On the other hand, policies allow banks to provide exchange settlement and related fund payment services based on transaction information collection and authenticity verification, relying on electronic transaction information. Therefore, prior to this enforcement action, some banks adopted very lenient verification policies for cross-border e-commerce foreign exchange settlement.

Following this enforcement action, numerous banks have tightened their foreign exchange settlement verification requirements.

II. Difficulties in Cross-Border Merchant Export Settlement

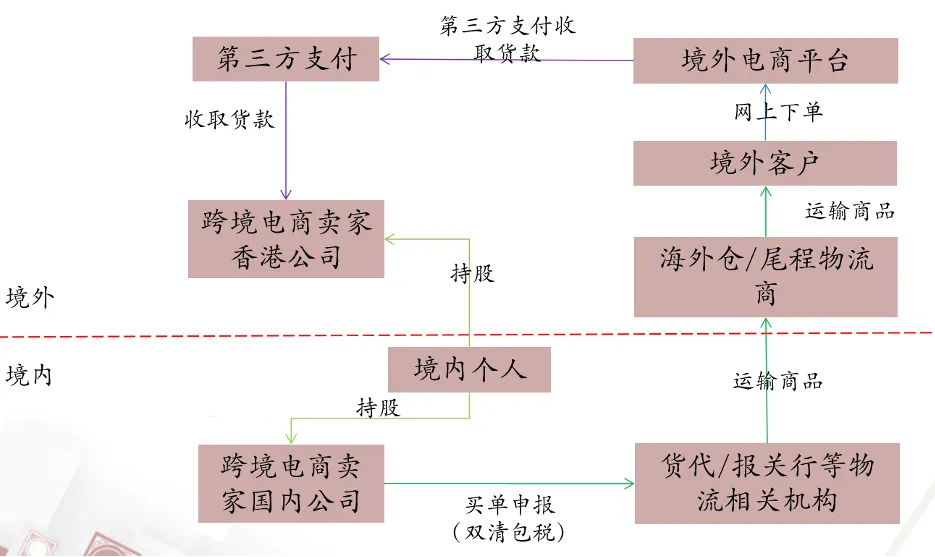

A. Foreign Exchange Compliance Issues Under Dual-Clearance Package-Tax Models

Many small and medium cross-border merchants adopt the “dual-clearance package-tax” model due to complex export customs and foreign exchange procedures. This model involves shipping agents or customs brokers arranging export customs in both countries, import customs, tariffs, and freight under a fixed price. This model is not recognized by customs or tax authorities. From a foreign exchange regulatory perspective, the consequence is that cross-border merchants cannot legally receive foreign exchange.

In this model, customs export information is not recorded in the customs monitoring system; merchants receive foreign exchange through controlled offshore company accounts, creating inconsistencies between logistics and capital flows.

B. Analysis of Illegal Foreign Exchange Trading

Due to inability to settle foreign exchange legally, some cross-border merchants resort to irregular methods such as borrowing others’ foreign exchange quotas or cross-border transfers. These methods constitute illegal foreign exchange trading. According to current regulations, entities within China can only settle foreign exchange through financial institutions with exchange settlement qualifications.

C. Round-Trip Investment Foreign Exchange Issues

For cross-border merchants using offshore company structures to receive export income, transferring funds back to the mainland requires compliance with special purpose company registration procedures under SAFE regulations.

III. Cross-Border E-commerce Foreign Exchange Compliance Strategies

Compliance cannot be achieved overnight. Enterprises must consider compliance costs, and “shock therapy” approaches may cause excessive harm. For small and medium cross-border e-commerce enterprises, phased and gradual compliance approaches should be adopted based on their circumstances.

The primary reason for inability to legally settle export income lies in failure to declare exports through proper channels, mainly to conceal income and avoid taxes.

For enterprises with established business scale, the risks and costs of non-compliant operations increase with size. Therefore, such enterprises should consider restructuring capital and logistics flows to achieve transparent export declarations.

About the Author

Zhang Jing is a Senior Partner at Longan Guangzhou, Director of the Corporate Law Committee, member of the Private Equity and Equity Investment Committee of Guangdong Province Lawyers Association, and a recognized emerging talent in foreign-related lawyering.