Credit Repair — A Path to Redemption for Those Who Have Lost Trust: Interpretation of Major New Regulations on Credit Information Repair

Credit Repair — A Path to Redemption for Those Who Have Lost Trust: Interpretation of Major New Regulations on Credit Information Repair

Attorney WU Zhiqin interprets the *Measures for the Administration of Credit Information Repair After Correction of Dishonest Acts (Trial)* (《失信行为纠正后的信用信息修复管理办法(试行)》) issued by the National Development and Reform Commission. The article points out that while China's current dishonesty punishment system has achieved significant results, the cost of punishment for non-malicious or minor dishonest actors is too high, making it urgent to establish a credit repair mechanism to combine punishment with education. The *Measures* clarify that credit repair is a legal right of credit subjects, aimed at lawfully removing or terminating the public disclosure of dishonest information, rather than erasing the illegal facts themselves. The *Measures* detail the scope, duration, conditions, and procedures for repairing serious dishonesty list information, administrative penalty information, and other dishonest information. Meanwhile, the *Measures* establish a central-local credit information coordination mechanism and set severe penalties for malicious acts such as submitting false materials or making seriously untrue credit commitments, including extended disclosure periods, restricted applications, and criminal liability. The author advises the public to strictly distinguish between "credit repair" and "credit reporting repair," engage legitimate and reliable institutions, and pay attention to the legal boundaries of commercial use of public data. The issuance of these *Measures* provides a lawful path for dishonest actors to reform, helps guide them to proactively correct illegal acts, and further optimizes the social credit system.

Table of Contents

Introduction

I. Legislative Background

II. Interpretation of Key Information in the Measures

III. Some Suggestions from the Author

Introduction

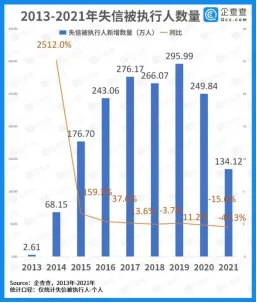

(1) Data on Dishonest Persons Subject to Enforcement in China

- Number of Dishonest Persons Subject to Enforcement from 2013 to 2021

(Data source: Qichacha)

The growth in the number of dishonest persons subject to enforcement has shown a downward trend, indicating that the social credit system previously established by the state has achieved initial results.

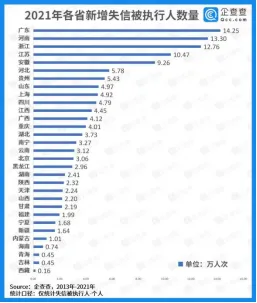

- Number of New Dishonest Persons Subject to Enforcement by Province in 2021

(Data source: Qichacha)

It can be seen that the highest numbers of new dishonest persons subject to enforcement are in Guangdong, Henan, and Zhejiang, while the lowest are in Tibet, Jilin, and Qinghai. This increase is related to the degree and activity of economic development.

(2) Current Legislative Status of China’s Dishonesty Punishment System

In recent years, China has established a strict dishonesty punishment system, producing strong deterrent and punitive effects across various industries. For example, the Several Provisions of the Supreme People’s Court on Publishing Information on Dishonest Persons Subject to Enforcement (《最高人民法院关于公布失信被执行人名单信息的若干规定》) established a “dishonesty blacklist” system to punish dishonest persons subject to enforcement by placing them on the blacklist for credit punishment. Additionally, financial, tax, and other institutions include relevant persons in credit blacklists and tax blacklists according to credit reporting regulations. As a vehicle for joint dishonesty punishment, the “dishonesty blacklist” plays an important role in promoting the construction of China’s social credit system, producing very significant effects in regulating and punishing dishonest behavior over a period of time.

However, through practical testing, it is not difficult to find that the dishonesty punishment system is simultaneously a double-edged sword. On the positive side, it helps promote the construction of a social credit system. Severe punishment systems have, to some extent, curbed the occurrence of illegal acts, making profit-seeking dishonest persons “want to but dare not” engage in dishonest behavior. On the negative side, for enterprises, being punished for dishonesty may subject them to restrictions in financial credit, stock issuance, bidding, applying for fiscal funds, enjoying tax benefits, and other aspects, significantly impacting their production and operations. For actors whose dishonest conduct is not serious, the cost of punishment may be disproportionately high, with significant restrictions on financing, bidding, travel, and consumption. The author believes that those who have money but refuse to repay and refuse to comply with court judgments (“deadbeats” or “laolai”) deserve their fate. However, for debtors who are “honest but unfortunate” — those who made investment mistakes or suffered from poor management, without malicious intent and willing to actively correct — the law should leave them opportunities to reform.

(3) Necessity of Establishing a Credit Repair Mechanism

In reality, most dishonest persons subject to enforcement lack awareness of credit repair and risk awareness. Due to the lack of clear institutional guidance, most persons subject to enforcement do not understand credit repair and the specific repair process, lacking effective positive incentive mechanisms to promote credit repair and voluntary performance.

There are also many profit-seeking intermediary institutions in society that operate under the guise of “eliminating and erasing dishonesty records” to seek improper benefits, causing many market entities and the public to lose a positive understanding of credit repair.

Therefore, rather than leaving most persons included in the dishonesty list in a passive state after inclusion, it is better to use this opportunity to help them establish the positive orientation of dishonesty punishment and honesty incentives, thereby establishing and improving a credit repair incentive system that guides dishonest persons to consciously and proactively correct dishonest behaviors and improve their performance capacity.

In 2019, the State Council issued the Guiding Opinions on Accelerating the Construction of a Social Credit System and Building a New Type of Credit-Based Supervision Mechanism (《关于加快推进社会信用体系建设构建以信用为基础的新型监管机制的指导意见》), which proposed exploring the establishment of a credit repair mechanism. On August 1, 2021, the State Administration for Market Regulation published three departmental rules and normative documents: the Measures for the Administration of the List of Seriously Illegal and Untrustworthy Market Entities (《市场监督管理严重违法失信名单管理办法》), the Provisions on the Public Disclosure of Administrative Penalty Information by Market Supervision and Administration (《市场监督管理行政处罚信息公示规定》), and the Measures for the Administration of Market Supervision and Credit Repair (《市场监督管理信用修复管理办法》), effective from September 1, 2021. On January 11, 2023, the National Development and Reform Commission issued the Measures for the Administration of Credit Information Repair After Correction of Dishonest Acts (Trial) (hereinafter the “Measures”), effective from May 1, 2023.

The issuance of the Measures gives dishonest persons a chance to reform. If a dishonest person is willing to sincerely correct, they have the right to credit repair according to law. The Measures cover the main methods of credit information repair, repair of information on the list of seriously dishonest entities, repair of publicly disclosed administrative penalty information, coordinated linkage of credit information repair, and supervision and management of credit information repair and credit education. The introduction of this repair mechanism helps dishonest persons extricate themselves from the sea of dishonesty earlier, promotes the flow and circulation of social resources, and encourages the proactive subjective initiative of dishonest entities to voluntarily and consciously correct illegal acts. Under the guidance of these Measures, dishonest persons can reform, and timely popularization of credit education can fundamentally strengthen the concept of good faith across society, reflecting the legislative principle and philosophy of combining leniency with severity and punishment with education.

(Source: National Development and Reform Commission official website)

II

Interpretation of Key Information in the Measures

(1) Clarification of the Rights of Credit Information Subjects and the Concept of Credit Information Repair

The Measures clearly stipulate that credit information repair is a legal right of credit subjects. Except for explicitly non-repairable situations, after correcting dishonest conduct and fulfilling relevant obligations, credit subjects may apply to the determining entity or collection institution to remove or terminate the public disclosure of dishonest information. However, the Measures clearly define that credit information repair refers to the removal or termination of publicly disclosed dishonest information, not the direct elimination or erasure of the illegal or dishonest conduct itself, as if it never occurred.

(2) Clarification of the Main Methods and Specific Procedures for Credit Information Repair

The methods of credit information repair include removal from the list of seriously dishonest entities, termination of public disclosure of administrative penalty information, and repair of other dishonest information. The Measures clearly define the scope, period, conditions, and procedures for these three methods.

The first method is repair of information on the list of seriously dishonest entities.

Applications for removal from such lists are handled by the determining entity. The “Credit China” website shall terminate the public disclosure of seriously dishonest entity list information within three working days from receiving the removal list shared by the determining entity.

The second method is repair of publicly disclosed administrative penalty information.

First, regarding the scope of publicly disclosed information: administrative penalty information imposed through summary procedures on legal persons and unincorporated organizations shall not be collected or publicly disclosed by credit platform websites; administrative penalty information involving warnings or criticism shall not be publicly disclosed; administrative penalty information on natural persons shall generally not be publicly disclosed on credit platform websites.

Second, regarding the period for administrative penalty information: the minimum public disclosure period is three months, and the maximum is three years. For administrative penalty information involving food, pharmaceuticals, special equipment, production safety, and fire safety, the minimum public disclosure period is one year.

Third, regarding remedial channels: the Measures provide remedial channels for legal persons or unincorporated organizations that disagree with an administrative penalty, where the administrative penalty has been lawfully revoked or modified, or where the legal person or unincorporated organization believes that the credit platform website has not timely updated its administrative penalty information or the information is incorrect.

Fourth, regarding conditions and procedures for early termination of public disclosure: after meeting three categories of conditions, an application may be made and materials submitted according to law, with review by the National Public Credit Information Center.

(3) Establishment of a Coordinated Linkage Mechanism Between Local and Central Authorities

Credit information systems are synchronously updated and consistent, protecting the legitimate rights and interests of credit subjects, improving the credibility and authority of credit information, and effectively resolving information conflicts.

(4) Clarification of Serious Consequences for Dishonest Conduct

The introduction of the credit information repair mechanism does not mean lowering standards or reducing requirements. For acts such as submitting false materials, making seriously untrue credit commitments, or being found by administrative authorities to have intentionally failed to fulfill commitments, severe punishment should be imposed. For example, relevant credit records will be publicly disclosed on the “Credit China” website for three years without early termination, and applications for credit information repair on credit platform websites will not be accepted for three years. If the conduct constitutes a crime, criminal liability will be pursued according to law. The Measures also regulate the illegal conduct of the National Public Credit Information Center, establishing a top-down honest and standardized system vertically and uniting the whole society for comprehensive social supervision horizontally, forming a precise and rigorous supervision system.

III

Some Suggestions from the Author

- “Credit repair” is different from “credit reporting repair,” and this distinction must be strengthened.

The Measures do not mention the “People’s Bank of China Credit Reference Center,” and the Measures are not applicable to “credit reporting repair.” There is much misleading information in the market, essentially exploiting the public’s urgent desire to delete adverse records for improper gain.

-

Credit subjects should proceed from their own needs and select legitimate and reliable institutions to handle credit repair matters.

-

The commercial use of public data has legitimacy but also boundaries. Certain internet credit reporting enterprises that harm the rights and interests of enterprises in their collection and publication of enterprise credit information may be held legally liable according to law.

Wu Zhiqin, Attorney

Partner, Beijing Long An (Shunde) Law Firm

First Batch of Financial Securities Professional Lawyers in Guangdong Province

Corporate Compliance Officer (Senior)

Member of the 14th and 15th Foshan Shunde District Committee of the Chinese People’s Political Consultative Conference

Supervisor, Foshan Shunde District New Social Stratum Association

Deputy Secretary-General, Shunde District Women Entrepreneurs Association

Attorney Wu Zhiqin has practiced since 2008 and specializes in corporate equity, corporate governance, investment and financing, and major complex commercial cases. Service values: customer-centric, legal and compliant, cost reduction and efficiency enhancement.

Hu Yongqi

Practice philosophy: “The life of the law lies not in logic, but in experience.”