Zhou Hongyi's RMB 9 Billion Divorce Settlement Sparks Controversy! Is It "Divorce for Cashing Out" or a Family Governance Arrangement?

Zhou Hongyi's RMB 9 Billion Divorce Settlement Sparks Controversy! Is It "Divorce for Cashing Out" or a Family Governance Arrangement?

Zhou Hongyi, the actual controller of 360 Security Technology, divorced his wife Hu Huan, with Hu Huan receiving 6.25% of the shares (worth nearly RMB 9 billion), sparking market质疑 of "divorce for cashing out." The company announced that control would not change and that Hu Huan committed to not reducing her holdings in the short term. The article analyzes that Hu Huan gave up equity in the holding company, holds Singapore permanent residency, and does not hold any position at 360, indicating that this event is actually a pre-planned wealth isolation and family governance arrangement by the Zhou Hongyi family, rather than a simple cashing out. This case provides an important reference for family governance and equity stability of listed companies.

First, there was the hundred-billion豪门 heir and stepmother’s drama at the shareholders’ meeting; now, a thousand-billion market cap company’s major shareholder couple’s divorce has been questioned as “divorce for cashing out”?

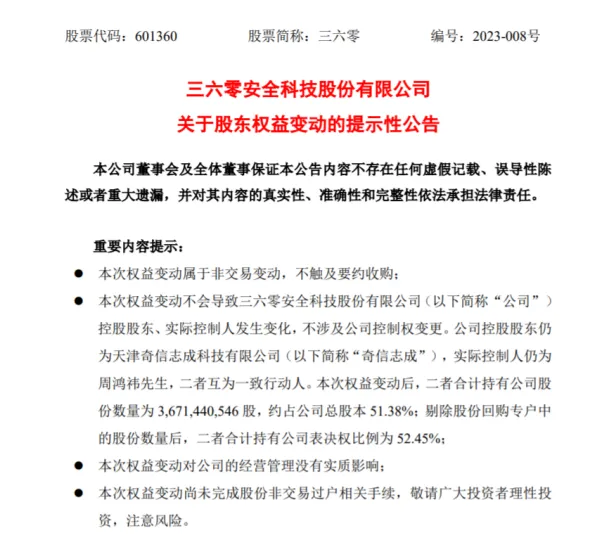

After the market closed on April 4, 360 (SH601360) issued an announcement on changes in shareholders’ equity. The company’s actual controller, Zhou Hongyi, and Hu Huan, after friendly negotiations, had completed the procedures for dissolving their marriage and made arrangements regarding share分割 and other matters. Zhou Hongyi proposed to transfer 6.25% of the company’s shares directly held by him to Hu Huan. This equity change would not result in any change in the company’s controlling shareholder or actual controller and would not involve a change in company control.

Figure: Announcement on Changes in Shareholders’ Equity

Amid the hype around the ChatGPT concept, 360’s stock price soared, more than doubling in just over two months. On April 4, the stock price hit a new two-year high, closing at RMB 20.08, with a market cap of RMB 143.5 billion. The shares Hu Huan received were worth nearly RMB 9 billion.

01

Model Couple’s Sudden Divorce Sparks Market Suspicion

The sudden news of a major shareholder’s divorce after market close unsettled minority shareholders and netizens, who纷纷 expressed their opinions and complaints on stock forums: “So you’re investing in stocks; they divorced just to cut you off,” “Reducing holdings through cashing out, morality is worthless in China,” “In the past there were fake divorces to sell houses, now there are naturally fake divorces to sell stocks”…

Facing market质疑, 360’s board secretary Zhao Luming couldn’t stay silent, posting on social media: “If anyone says I came up with this cashing out strategy for the boss, I’ll fight them—you’re insulting my professional ability.”

Zhou Hongyi and Hu Huan were a married couple with a relatively stable relationship and no scandals. They could be considered a “model couple” among listed companies. Whether this divorce was truly due to relationship breakdown or other reasons is certainly unknown to minority shareholders and netizens, and whether the board secretary truly knows is probably unclear even to him. In fact, whether Zhou Hongyi’s divorce case is a “divorce for cashing out” is not that important. What merits more consideration is why his divorce caused such a significant impact—the market has already given investors many lessons.

02

Frequent Cases of Listed Company Shareholders Cashing Out Through Divorce

In recent years, divorce cases involving shareholders of A-share listed companies have occurred frequently. Apart from a few court-decided divorces, such as Sai Teng Shares (SH603283) Zeng Hui and Sun Feng’s divorce, and Laishuo Tongling (SH603900) Shen Dongjun and Ma Qiao’s divorce, most other divorce cases were amicable separations reached through divorce agreements, including equity分割 of listed company shares. These include Kunlun Wanwei (SZ300418)‘s RMB 7 billion天价 settlement, Mengjie Shares (SZ002397)‘s RMB 1 billion settlement, Yixintang (SZ002727)‘s RMB 2 billion settlement, and Kangtai Biological (SZ300601)‘s RMB 23.5 billion天价 settlement.

After divorce equity分割, cases where one or both parties reduce their holdings and cash out frequently occur, with Kangtai Biological’s Yuan Liping’s reduction being the most classic: In May 2020, Kangtai Biological announced that actual controller Du Weimin had divorced his Canadian wife Yuan Liping. Du Weimin transferred 161 million shares directly held by him to Yuan Liping, valued at approximately RMB 23 billion at market price, setting an A-share “sky-high divorce” record. Half a year after the divorce, as Kangtai Biological’s stock price continued to inflate amid the COVID-19 vaccine concept, Yuan Liping began her cashing out journey, successively reducing her Kangtai Biological holdings through block trades, centralized竞价, and协议 transfer, with the highest average sale price reaching RMB 194.28. By the end of 2022, Yuan Liping had cashed out over RMB 3 billion in total. Along with Yuan Liping’s frequent reductions and those of other major shareholders and executives, Kangtai Biological’s stock price fell to RMB 31.57 at the close on April 4, with a market cap of only RMB 35.2 billion.

03

1. Hu Huan Only Took Part of 360’s Circulated Shares and Gave Up Equity in Qixin Zhicheng

Relevant announcements and information show that 360’s largest shareholder is Tianjin Qixin Zhicheng Technology Co., Ltd., holding 3.297 billion shares worth over RMB 60 billion. Qixin Zhicheng’s largest shareholder and actual controller is Zhou Hongyi, holding 17.39% of the company’s equity. In the divorce between Zhou Hongyi and Hu Huan, this portion should have been subject to distribution. Public information shows that Hu Huan gave up her rights to this part.

Figure: Major Shareholders of 360 Security Technology Co., Ltd.

Figure: Major Shareholders of Tianjin Qixin Zhicheng Technology Co., Ltd.

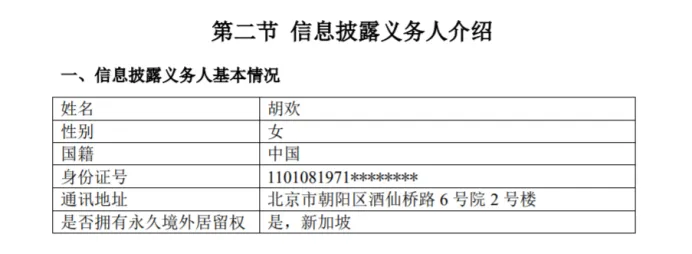

2. Hu Huan Has Obtained Singapore Permanent Residency

On April 5, 360 Group issued an announcement on changes in shareholders’ equity and simplified equity change reports for Zhou Hongyi and Hu Huan. Their respective simplified equity change reports show that Zhou Hongyi was born in 1970. Hu Huan is one year younger than Zhou Hongyi. Hu Huan’s simplified equity change report shows that she has Singapore permanent overseas residency.

Figure: Simplified Equity Change Report (Hu Huan)

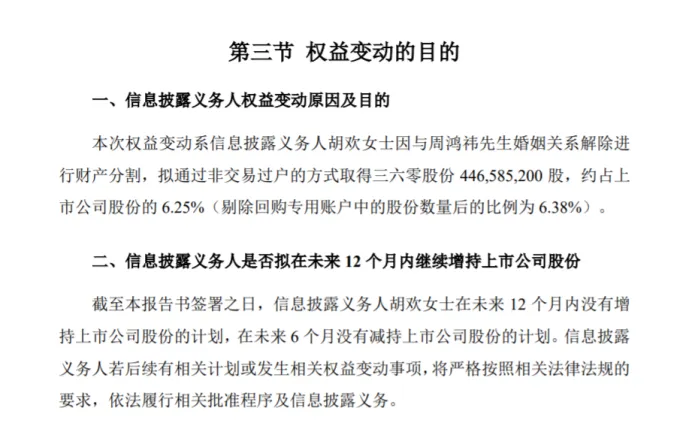

3. Hu Huan Has No Plan to Reduce Listed Company Shares Within the Next 6 Months

Relevant announcements show that Ms. Hu Huan has no plan to increase her holdings of listed company shares within the next 12 months and no plan to reduce her holdings of listed company shares within the next 6 months. If there are subsequent plans or relevant equity change matters, she will strictly comply with relevant laws and regulations and fulfill relevant approval procedures and information disclosure obligations.

Figure: Simplified Equity Change Report (Hu Huan)

Hu Huan holds approximately 6.25% of 360’s shares. If she wishes to reduce her holdings early, she would need to provide pre-disclosure. If Hu Huan changes her plans in the future and wants to reduce her holdings as soon as possible, she can do so by fulfilling relevant procedures and making pre-disclosure.

04

View of the Common Family Governance Center

We believe that this RMB 9 billion divorce case between Zhou Hongyi and Hu Huan may be a relatively classic family governance case worthy of study and reference. While everyone focuses on whether it is a “fake divorce, real reduction,” in fact, Zhou Hongyi should have been planning and arranging family governance long ago, and this divorce is merely one step in the adjustment of his family governance structure and wealth arrangement. This is mainly manifested in the following aspects:

Hu Huan previously co-founded 3721 with Zhou Hongyi but has never appeared on 360’s key personnel list. This announcement also shows that Ms. Hu Huan does not hold any position in 360 Group or its subsidiaries. The relationship between Hu Huan and 360 is so clean; this should have been arranged long before 360’s listing. Meanwhile, the enterprises controlled by Zhou Hongyi and Hu Huan各自 have no交叉 or关联 relationships. Hu Huan is primarily engaged in investment business and is quite adept in the capital market, cooperating with top capital such as Sequoia, CDH, and Gaorong, achieving great success in investments such as Xunyou Technology (SZ300476). Clear equity,明確 control, and complete risk isolation mechanisms are core elements of family business governance. The Zhou Hongyi family’s practice of planning ahead in this way is commendable.

Hu Huan’s Singapore identity also indicates that the Zhou Hongyi family’s family governance arrangements in recent years have included advance identity planning. Singapore is currently the most favored destination for ultra-wealthy individuals, with its immigration门槛 rising year by year—without billions in assets, Singapore immigration is not worth considering. When Hu Huan obtained her Singapore identity is unknown; public information shows that she obtained it after December 2017. Could it be a recently acquired身份, and is it related to this divorce?

Family governance is the foundation of家族治理. Whether family relationships are properly handled affects the rise and fall of the family and family business. If a listed company’s controlling shareholder’s divorce, particularly property分割, is not handled well, it can easily trigger protracted marital battles, with equity分割 being the core issue in divorce property处理. Whether this RMB 9 billion divorce case between Zhou Hongyi and Hu Huan is, as we have analyzed, a classic and successful family governance case, time will tell. Let us wait and see.