Key Points and Analysis of the Third Draft Company Law Revision from Stakeholder Perspective

Key Points and Analysis of the Third Draft Company Law Revision from Stakeholder Perspective

Ke Cheng, Longan Bay Area Legal Research Institute, 2023-12-26

Introduction

Company Law is a fundamental law in China’s civil and commercial fields, playing a pivotal role under the socialist market economic system. With the Civil Code already promulgated and implemented, revising Company Law has become a legislative priority. However, Company Law has complexity: it has both public and private law attributes, combines organizational and transactional law characteristics, contains both substantive and procedural content, and its mandatory versus default provisions are difficult to distinguish. Company Law regulates various company types including limited liability companies, joint-stock companies, and state-owned enterprises. This means Company Law revision is a systemic project affecting all aspects. The current Company Law was promulgated in 1993, later revised five times in 1999, 2004, 2005, 2013, and 2018. Since 2021, Company Law has entered its sixth revision, with the first and second drafts reviewed by the NPC Standing Committee in December 2021 and December 2022 respectively, and the third draft reviewed and published for public comment by the NPC Standing Committee on September 1, 2023. This article analyzes this round of Company Law revisions to explore why and how Company Law should be revised, and from the stakeholder perspective, how the revised Company Law will affect commercial activity parties.

I. Reasons for Company Law Revision

According to the NPC Standing Committee’s official statement in “Explanatory Document on Company Law Revision Draft,” modification is needed for deepening state-owned enterprise reform and improving the modern enterprise system with Chinese characteristics; continuously optimizing the business environment and stimulating market innovation vitality; improving property rights protection systems and strengthening property rights protection according to law; and improving capital market basic systems and promoting healthy capital market development.

The official statement reveals the intended goals of Company Law modification. From a practical perspective, Company Law modification is also necessary due to lags and deficiencies in the current Company Law’s practical operation, facing issues such as weakened protection of small and medium shareholders and creditor interests, rigid and dysfunctional corporate governance mechanisms, failed internal supervision, incomplete shareholder exit mechanisms, weak Company Law norms’ justiciability, and inflexible capital systems. Responding to problems exposed in Company practice through revision is truly necessary.

II. Direction of Company Law Revision

Company Law revision bears high expectations, but modifying Company Law is not just patching system loopholes based on symptoms; rather, it should first clarify the Company Law system and then systematically inspect and improve based on scientific system design.

As mentioned, Company Law has complexity but also distinct logical脉络. Company Law’s private law attributes require the state to fully respect and encourage company autonomy to stimulate market subject enthusiasm and creative spirit, thus clearly separating state and market subjects: on one side is the realm of market freedom and company autonomy, on the other is the aloof observation of public power. At the market end, creditors interact with company autonomy-related parties, but core is creditors’ hope to use the company to achieve commercial value and尽力避免自身权益遭受公司自治相关方的侵害. Within the company autonomy system, the company as a legally fictional subject already has consensus on independent personality. Based on the company’s independent personality, company self-governance should center on the company. Although directors, supervisors, and senior management collectively (“Dong Ji Gao”) are directly or indirectly derived from shareholders and shareholder meetings they control, once generated, Dong Ji Gao should belong to the company’s Dong Ji Gao rather than shareholders’ Dong Ji Gao. Like shareholder contributions, once completed, shareholder-contributed property should be company property rather than shareholders’ private property.

Understanding this, it is easy to comprehend why the three drafts of Company Law all deleted the expression “Board of Directors is responsible to the Shareholders’ Meeting” from Article 46 of the current Company Law. The heated debate on whether Company Law is “Shareholders’ Meeting Centralism” or “Board of Directors Centralism” is unnecessary. “Shareholders’ Meeting Centralism” and “Board of Directors Centralism” were originally concepts refined for convenience of expression and communication but are not rigorous legal concepts; their connotations and extensions have not obtained absolute consensus. Using non-rigorous concepts refined for expression convenience and applying them inversely to specific systems, thereby triggering concept disputes, is inappropriate. Opposing the distortion of “Shareholders’ Meeting Centralism” and “Board of Directors Centralism” expressions in Company Law, both Shareholders’ Meeting and Board of Directors are components of corporate governance; how company power is distributed between them should comprehensively consider corporate governance effectiveness, governance costs, and protection of various parties’ interests. The best corporate governance outcome should be shareholders, shareholders and Dong Ji Gao, creditors forming joint force to jointly propel the company to go far and solid.

Shareholder interests not effectively guaranteed will suppress shareholders’ entrepreneurship and innovation motivation; creditor interests not effectively guaranteed will cause the company to gradually lose capital market financing channels, becoming water without source; Dong Ji Gao responsibility design improperly (mismatch of power and responsibility) will either cause Dong Ji Gao to shrink from action or damage public enrichment private, infringing shareholder, company, and others’ interests.

Therefore, the direction of Company Law revision is to supply sufficient and quality institutional mechanisms, through refined institutional design, promote consistency between all parties’ power and responsibility, and achieve balance and coordination of all parties’ interests. Specifically, it means grasping the boundary between public power intervention and company autonomy, strictly examining and clarifying mandatory and default provisions in Company Law, reducing practical identification disputes; focusing institutional design on four main subjects: shareholders, company, Dong Ji Gao, and creditors; and focusing on adjustment of seven groups of legal relationships: between shareholders, between shareholders and company, between shareholders and Dong Ji Gao, between company and Dong Ji Gao, between creditors and shareholders, between creditors and company, and between creditors and Dong Ji Gao.

III. Key Points and Analysis of Third Draft from Stakeholder Perspective

Law’s normative functions include guidance, evaluation, prediction, education, and coercion. Once passed, the third draft’s revised content will have significant impact on commercial fields, worthy of full understanding by different stakeholders to make advance commercial arrangements.

A. Key Points and Analysis from Creditor Perspective

Shareholders bear limited liability to the company to the extent of their contributions. Company guarantees to creditors mainly depend on two aspects: the company’s original income from shareholder contributions, and the company’s operational income from asset appreciation. Current Company Law has deficiencies in protecting both company’s original income and operational income. The third draft summarizes practical experience, focusing on these two aspects for revision.

1. Revised Clauses Protecting Company’s Original Income

The third draft’s revised clauses around company’s original income further clarify contribution periods, contribution subjects, capital reduction, withdrawal of contributions, and sponsor liability, solving questions of stability of company’s original income total, responsible subjects when not fulfilled, and accelerated fulfillment rules, forming a relatively complete protection system.

2. Perfecting Shareholder Contribution Acceleration Due System

After 2013 Company Law introduced the capital subscription system, whether shareholder contributions can accelerate due became a controversial topic. The 2019 Ninth Civil Minutes Article 6 clarified shareholders have term interests, with only two exception circumstances. The third draft Article 53 deletes the Ninth Civil Minutes’ restrictions, providing that when “company cannot repay due debts,” the company or creditors with matured claims may require unpaid shareholders to pay contributions in advance. This revision makes it easier for creditors to pursue shareholders’ contribution obligations and ensures company’s original income is smoothly fulfilled.

3. New Rules for Equity Transfer Before Contribution Due Date

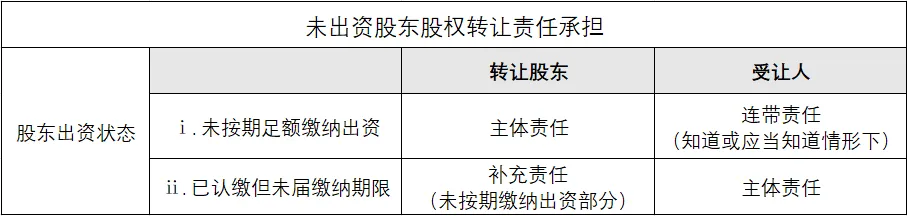

Transferring equity before the contribution due date easily allows shareholders to transfer to less creditworthy third parties to evade fulfillment responsibility. The third draft Article 88 clarifies transferees bear contribution obligations, with transferors bearing supplementary responsibility for transferees’ unpaid contributions.

4. New Compensation Liability for Illegal Capital Reduction

Capital reduction will abruptly reduce creditors’ expected company’s original income, affecting creditworthiness and solvency. The third draft Article 226 clearly provides that shareholders and responsible Dong Ji Gao shall bear compensation liability for losses.

B. Key Points and Analysis from Shareholder Perspective

1. Changes to One-Person Company Rules

The third draft deletes special provisions on one-person limited liability companies in the current law. Shareholders now have more flexibility in choosing one-person companies.

2. Adding Equity and Creditor’s Rights as Contribution Methods

The third draft Article 48 newly adds “equity and creditor’s rights” as contribution methods, legally confirming these two methods.

3. Five-Year Contribution Period for Limited Liability Companies

The most discussed clause—shareholders must fully pay contributions within five years—represents significant discussion and controversy during the revision process.

4. New Shareholder Forfeiture System for Contribution Refusal

This system further perfects shareholder contribution rules based on the five-year payment requirement.

5. Perfecting Shareholder Information Right Rules

The third draft adds rights to inspect and copy shareholder registers and accounting vouchers, and to entrust accounting and law firms for inspection.

C. Key Points and Analysis from Dong Ji Gao Perspective

Compared to creditors who are distant from company operations and shareholders who can only indirectly manage through shareholders’ meetings or electing/changing directors and supervisors, Dong Ji Gao are direct subjects of company operations and management. The third draft expands board authority while also increasing Dong Ji Gao responsibilities.

1. Expanding Board Authority Clauses

The third draft allows audit committees within boards and creates an authorized capital system.

2. Increasing Supervision of Directors and Senior Management

New rules include removal without cause system and external liability for directors and senior management.

3. Perfecting Dong Ji Gao Duty Clauses

New provisions clarify loyalty and diligence duties, “shadow director and executive” liability, and liability for illegal profit distribution.