Under the New Company Law, How Can Minority Shareholders Deal with Willful Majority Shareholders?

Under the New Company Law, How Can Minority Shareholders Deal with Willful Majority Shareholders?

The new Company Law strengthens the protection of minority shareholders' rights and interests through multiple institutional innovations to effectively check the abuse of controlling power by majority shareholders. First, it significantly expands shareholders' right to inspect, clarifying that shareholders can inspect accounting vouchers, entrust professional institutions to assist in auditing, and extending the inspection scope to wholly-owned subsidiaries, providing the information foundation for minority shareholders to monitor company finances and operations. Second, it strengthens the fiduciary duties of directors, supervisors, and senior management, introducing the "de facto director" rule and strictly regulating related transaction procedures and disgorgement of profits, effectively lowering the threshold and difficulty of proof for minority shareholders to initiate derivative lawsuits. Third, in response to the dilemma where litigation proceeds belong to the company, the new law creates a minority shareholder mandatory exit right, allowing them to require the company to repurchase their equity at a reasonable price when the controlling shareholder abuses rights. The article emphasizes that although post-event legal remedies are increasingly robust, minority shareholders should focus more on pre-investment agreement structure design and active participation in corporate governance, using ex-ante prevention to replace ex-post博弈, to more effectively protect their lawful rights and interests.

I. Introduction

In a company, where there are majority shareholders, there are inevitably minority shareholders (for convenience, “majority shareholders” in this article refer to shareholders who hold more than half of the voting rights or the power to appoint more than half of the directors, i.e., shareholders with control over the company; “minority shareholders” refer to shareholders without control over the company). Under the institutional arrangement of capital majority rule, majority shareholders generally control the appointment of the board of directors, the board of supervisors, and senior management. Precisely because of the dominant position of majority shareholders in the company, when majority shareholders are willful, minority shareholders may be at their mercy.

On December 29, 2023, the revised Company Law (hereinafter “New Company Law”) was enacted. The New Company Law establishes mechanisms such as minority shareholders’ mandatory exit right and strengthens the fiduciary duties of directors, supervisors, and senior management, aiming to balance the interests between minority and majority shareholders. So, under the New Company Law, when facing majority shareholders who harm the company and minority shareholders’ interests, how can minority shareholders protect their rights?

II. Under the New Company Law, How Can Minority Shareholders Check Willful Majority Shareholders?

(1) Exercising the Right to Inspect

As is well known, sunlight is the best disinfectant. In sunlight, most demons and monsters will have nowhere to hide.

Ensuring shareholders’ right to inspect is intended to make the company operate in the sunlight and is also an important prerequisite for shareholders to exercise their rights. Under the 2018 version of the Company Law (hereinafter “Old Company Law”), although there were provisions protecting shareholders’ right to inspect, they were not entirely reasonable. We are pleased to see that the New Company Law has made necessary revisions to the provisions protecting shareholders’ right to inspect under the Old Company Law.

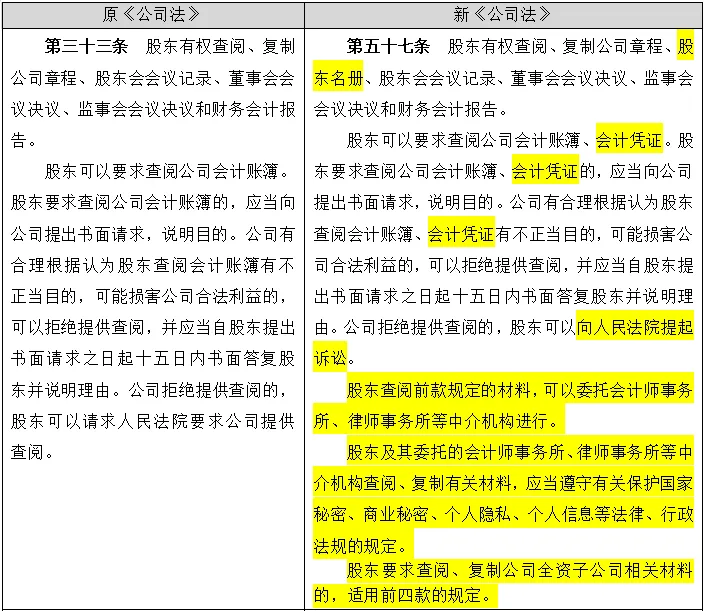

From the above table, the main revisions made by the New Company Law regarding shareholders’ right to inspect are as follows:

1. Clarifying that shareholders may inspect not only accounting books but also accounting vouchers.

Under Article 33 of the Old Company Law, shareholders could request to inspect the company’s accounting books. According to Article 15 of the “Accounting Law of the People’s Republic of China” (2017 Amendment), accounting books include general ledgers, subsidiary ledgers, journals, and other auxiliary books. However, accounting books are merely the intermediate link connecting accounting vouchers and accounting statements. Accounting books are generally presented in a format similar to an Excel spreadsheet. That is, by only inspecting accounting books, shareholders cannot verify the authenticity of a particular accounting item. Only by inspecting accounting vouchers can shareholders understand the company’s operations and financial condition.

Article 33 of the Old Company Law only provided that shareholders could inspect the company’s accounting books but did not explicitly state that shareholders could inspect accounting vouchers. If strictly interpreted according to the literal meaning, shareholders’ right to inspect would not be effectively guaranteed. For this reason, in judicial practice, courts have inconsistent standards regarding whether shareholders can inspect accounting vouchers. For example, in the case (2019) Zui Gao Fa Min Shen No. 6815, the guiding opinion of the Beijing Higher People’s Court held that shareholders of a limited liability company have the right to inspect the company’s accounting books, including记账 vouchers and原始 vouchers. However, the Supreme People’s Court held a截然相反 view.

The New Company Law clarifies that shareholders may inspect both accounting books and accounting vouchers. This will help end the situation of inconsistent judicial standards regarding the scope of shareholders’ right to inspect in practice, and better protect the rights of minority shareholders.

2. Clarifying that shareholders may entrust accounting firms, law firms, and other intermediary institutions to conduct inspections.

Article 10(2) of the “Provisions of the Supreme People’s Court on Several Issues Concerning the Application of the Company Law of the People’s Republic of China (IV) (2020 Revision)” (hereinafter “Judicial Interpretation (IV) of the Company Law”) provides: “Where a shareholder, based on an effective judgment of the people’s court, inspects the company’s documents and materials, in the presence of the shareholder concerned, accountants, lawyers, or other professionals of intermediary institutions who have confidentiality obligations according to law or professional conduct standards may assist in the inspection.” Under this provision, after the people’s court has made an effective judgment on the right to inspect and in the presence of the shareholder concerned, accountants, lawyers, and other professionals of intermediary institutions may assist in the audit.

The New Company Law has removed the above-mentioned restrictive conditions, i.e., shareholders may directly entrust accounting firms, law firms, and other intermediary institutions when asserting their right to inspect.

3. The scope of shareholders’ right to inspect extends to the company’s wholly-owned subsidiaries.

Before the promulgation of the New Company Law, when majority shareholders wanted to circumvent minority shareholders’ rights such as the right to inspect and voting rights, a common method was—the company established subsidiaries and transferred company assets to the subsidiaries. At the subsidiary level, the parent company controlled by the majority shareholder exercised shareholder rights, and minority shareholders could not directly enjoy the right to inspect the subsidiaries, nor could they participate in the subsidiaries’ operational decisions.

After the implementation of the New Company Law, minority shareholders may directly exercise the right to inspect the company’s wholly-owned subsidiaries. The practice of majority shareholders setting up subsidiaries to circumvent minority shareholders will be significantly curbed.

In summary, the New Company Law has made rather robust institutional designs to protect minority shareholders’ right to inspect in order to balance the rights and interests between minority and majority shareholders. However, it should be noted that the boundary between respecting company autonomy and necessary judicial intervention has always been difficult to clearly define. For this reason, the above provisions in the New Company Law protecting shareholders’ right to inspect are only effective to a general extent and cannot fully guarantee minority shareholders’ right to inspect.

The reason is that the company’s finance department is itself a back-office department. The finance department’s preparation of complete and accurate accounting vouchers and financial statements depends on the authenticity and timeliness of the operational data fed back by front-office departments such as procurement, warehousing, production, and sales. When the company’s internal control mechanism is defective, solely relying on inspecting accounting books and accounting vouchers is insufficient to confirm the authenticity of the financial statements.

For example, in manufacturing enterprises with complex business chains, the calculation and transfer of cost expenses and revenues often rely on ERP systems. However, ERP systems are not within the scope of shareholders’ right to inspect under the New Company Law, and minority shareholders cannot confirm whether the ERP system is genuinely implemented in the company’s front-office departments. Therefore, if the data entered into the ERP system itself is erroneous or flawed, minority shareholders and their entrusted professional institutions will find it difficult to identify the authenticity of profit data in the company’s financial statements by only inspecting accounting vouchers.

In a word, for minority shareholders to obtain more adequate protection regarding the right to inspect, it is inseparable from ex-ante top-level design and personalized corporate governance arrangements.

(2) Exercising Shareholder Derivative Litigation Rights

If majority shareholders want to harm the company for personal gain, they rely on the tolerance or cooperation of the company’s directors, supervisors, and senior management (of course, for most non-public companies, the majority shareholders themselves are the directors, supervisors, and senior management).

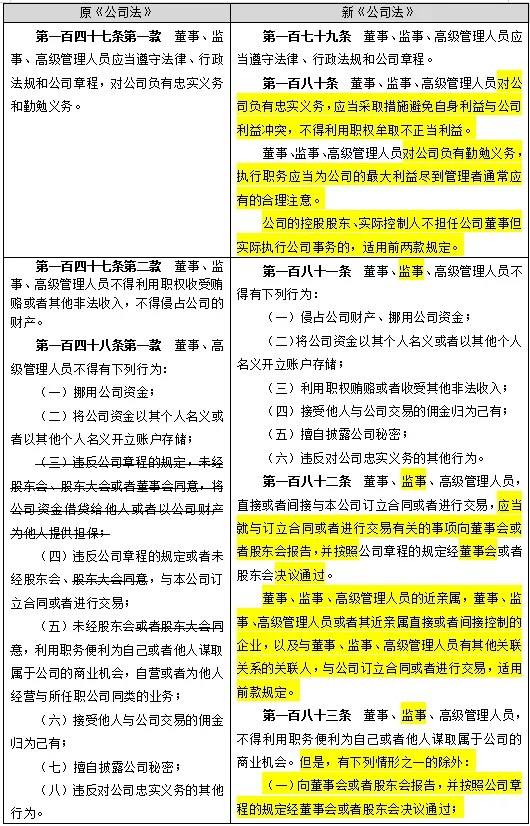

To balance the interests between majority and minority shareholders, the level of fiduciary duties owed by directors, supervisors, and senior management to the company needs to be improved, which is precisely a highlight of the New Company Law’s revisions.

From the above comparison table, the New Company Law mainly makes the following provisions to improve the level of fiduciary duties of directors, supervisors, and senior management:

1. Adding rules for identifying de facto directors.

If the company’s controlling shareholder or actual controller does not serve as a director but actually executes company affairs, they must also comply with the fiduciary duties of directors. That is, if a majority shareholder uses a “shell” and appoints someone else as a nominal director while actually executing company affairs themselves, they owe fiduciary duties to the company.

2. Directors, supervisors, senior management, and their related parties must report transactions with the company, which must be approved by the shareholders’ meeting or board of directors.

A common method for majority shareholders to divert company profits is through related transactions with unreasonable pricing.

Under Article 21 of the Old Company Law, if the company’s controlling shareholder, actual controller, or directors, supervisors, or senior management use related relationships to cause losses to the company, they must bear compensation liability. However, this provision has limited deterrent effect on majority shareholders. This is because minority shareholders not only need to prove that a related transaction exists between the majority shareholder and the company but also need to prove that the company suffered losses—a significant difficulty of proof.

However, under the New Company Law, majority shareholders will face greater difficulty in diverting company profits through related transactions. First, the subjects required to report related transactions include not only the majority shareholder, directors, supervisors, senior management, and their close relatives, but also enterprises directly or indirectly controlled by the above persons, and other related parties having other related relationships with directors, supervisors, and senior management. Second, such related transactions must, according to the company’s articles of association, be approved by the company’s shareholders’ meeting or board of directors, and related directors must abstain from voting. Third, if the foregoing reporting obligations are not fulfilled, the income from such related transactions belongs to the company.

In summary, under the New Company Law, if minority shareholders suspect that the majority shareholder has engaged in conduct harming the company’s interests, they may first assert their right to inspect. Then, based on the results of exercising the right to inspect, three situations can be discussed:

Situation 1: After exercising the right to inspect, minority shareholders discover transactions between the company and the company’s directors, supervisors, senior management, or the majority shareholder (who actually performs director duties) and their close relatives and other related parties, and such transactions have not been reported. In this situation, minority shareholders may claim that the income obtained by such related parties from the company should belong to the company (after fulfilling the前置 procedures, they may initiate a derivative lawsuit).

Situation 2: After exercising the right to inspect, minority shareholders do not find transactions between the company and the company’s directors, supervisors, senior management, or the majority shareholder (who actually performs director duties) and their close relatives and other related parties, but they find suspicious transactions (e.g., disposal of assets at low prices or purchase of assets at high prices, or substantial management expenses). In this situation, minority shareholders may submit relevant vouchers copied during the audit as初步 evidence and require the majority shareholder (if the majority shareholder themselves is a director, supervisor, senior manager, or de facto director) to prove the reasonableness of their conduct (there is no一刀切 standard for the plaintiff’s burden of proof in derivative lawsuits, which will not be detailed in this article).

Situation 3: After exercising the right to inspect, minority shareholders find neither related transactions nor suspicious transactions. In this situation, it is possible that minority shareholders are overly worried, or the company’s financial level is too high and irreproachable. At this point, minority shareholders need to find other ways to obtain evidence that the majority shareholder is harming the company’s interests.

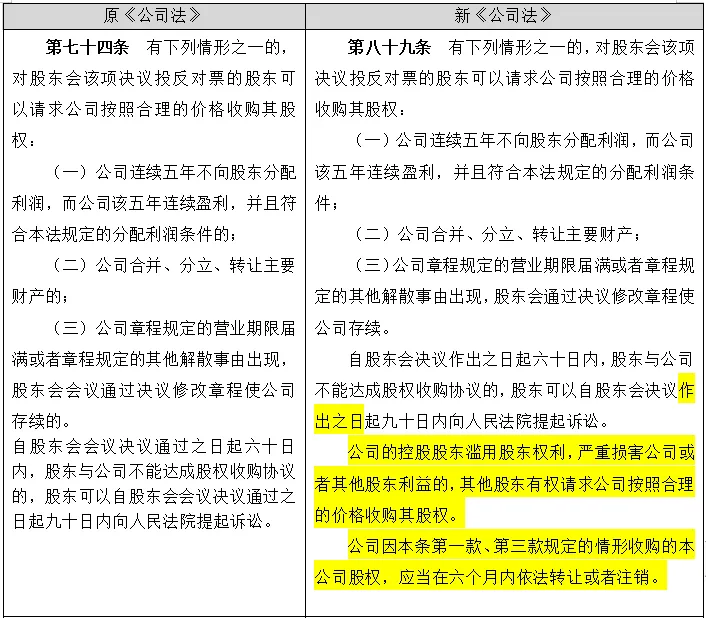

(3) Mandatory Exit Right

Even if minority shareholders succeed in a derivative lawsuit, the proceeds from the victory will flow to the company, and minority shareholders will not directly benefit. If they encounter a “miserly” company that refuses to distribute dividends, minority shareholders will find it difficult to obtain dividends or have a reasonable exit pathway.

According to Article 15 of Judicial Interpretation (IV) of the Company Law, where the majority shareholder abuses shareholder rights, minority shareholders may request the court to order mandatory dividends. However, even if the court orders mandatory dividends, it is unlikely to order the distribution of all the company’s undistributed profits to shareholders.

Given that minority shareholders and majority shareholders are already disaffected, it becomes particularly difficult for minority shareholders to protect their investment interests. They may even face constant harassment from the majority shareholder. For minority shareholders at this point, it is better to endure short-term pain and exit at a reasonable price—the best option for rights protection. The New Company Law, based on this consideration, provides that minority shareholders have the right to mandatory exit.

From the above comparison table, under the New Company Law, when facing a majority shareholder who abuses shareholder rights, if minority shareholders choose not to seek mandatory dividends, they may instead require the company to repurchase their equity at a reasonable price. This institutional design is more conducive to protecting minority shareholders’ rights.

III. Conclusion

The journey from “brotherly partnership” to “enemy-style breakup” for shareholders typically goes through the psychological process of “shared aspirations, sharing hardships, sleeping in the same bed with different dreams, and mutual destruction.”

During this process, the majority shareholder controls the company and is often initially emboldened. However, minority shareholders should still bravely assert their rights. In cases handled by the author, there are many examples where the majority shareholder proactively sought negotiation after the minority shareholder asserted their right to inspect. This is because if a company’s majority shareholder is willful, it is hard to avoid having various skeletons in the closet. When faced with a minority shareholder asserting their right to inspect, the majority shareholder, fearing reprisals, has no choice but to seek reconciliation.

For minority shareholders, compared to the post-event remedies provided by company law for protecting minority shareholders’ rights, the ex-ante design of shareholder agreements and partnership mechanisms, as well as avoiding information asymmetry through active participation in company management, are more effective in protecting their rights and interests. After all, investing and then sitting back to do nothing, waiting for dividends every year—such a rosy scenario exists mostly only in dreams.