Why Equity Investments Become "Money Down the Drain": —A Practical Perspective on Profit Distribution Plans and Related Provisions Under the Judicial Interpretation (IV) of the Company Law

Why Equity Investments Become "Money Down the Drain": —A Practical Perspective on Profit Distribution Plans and Related Provisions Under the Judicial Interpretation (IV) of the Company Law

Attorney HUANG Enlin and XU Hongpeng focuses on the judicial recognition standard for "shareholders' resolution specifying a specific profit distribution plan" under Articles 14 and 15 of the Judicial Interpretation (IV) of the Company Law. Through analysis of practical cases, the article points out that courts strictly examine the formal and substantive requirements of resolutions: oral dividend agreements are generally not recognized; if the company's articles of association specify a specific distribution plan, they may be referenced; general meeting documents must satisfy properly qualified signatories, procedural compliance, and specific content (including amount, time, and method) to potentially constitute an effective resolution. Given the extremely high failure rate of dividend lawsuits in practice due to the lack of formal written resolutions, the article recommends that shareholders must ensure written documentation, ensure voting procedures are lawful, and clearly define the core terms of distribution to effectively protect their dividend rights.

Background

One of the main purposes[1] of shareholders (or equity investors) investing in a company (the investment target) is to seek capital appreciation and company profitability after the invested company has engaged in production and operation activities for a certain period, and to obtain corresponding dividends. Therefore, it can be said that whether dividends are realized and the effect of their realization is one of the most concerned issues for shareholders and investors.

Under Chinese law, limited liability companies have both “capital” and “personal” attributes. The profit distribution of a limited liability company also has a high degree of “autonomy.” The shareholders of a limited liability company may determine according to law how the company distributes profits and whether to distribute profits within a certain period. However, in practice, some controlling shareholders or actual controllers of companies, in order to maximize their own interests, often take advantage of their controlling position by refusing to distribute profits for extended periods when the company has profits, seriously harming the interests of minority shareholders. Coupled with the fact that, in practice, limited liability companies, especially non-state-controlled ones, often have irregular corporate governance and neglect the importance of lawful and compliant corporate governance, minority shareholders of limited liability companies are often at a disadvantage when facing the above difficulties.

To regulate the above issues, the Company Law and relevant judicial interpretations have made corresponding provisions. Article 74 of the Company Law provides that if a company has not distributed profits to its shareholders for five consecutive years, but the company has been profitable for those five consecutive years and meets the conditions for profit distribution under the Company Law, shareholders who voted against the resolution at the shareholders’ meeting may request the company to repurchase their equity at a reasonable price. Articles 14 and 15 of the “Provisions of the Supreme People’s Court on Several Issues Concerning the Application of the Company Law of the People’s Republic of China (IV)” (hereinafter “Judicial Interpretation (IV) of the Company Law”) provide: Where a shareholder submits an effective shareholders’ meeting resolution specifying a specific distribution plan and requests the company to distribute profits, if the company refuses to distribute profits and its defense that the resolution cannot be implemented is not established, the people’s court shall order the company to distribute profits to the shareholder according to the specific distribution plan specified in the resolution. Where a shareholder does not submit a shareholders’ meeting resolution specifying a specific distribution plan and requests the company to distribute profits, the people’s court shall dismiss the claim, unless the failure to distribute profits is caused by the abuse of shareholder rights in violation of legal provisions, causing losses to other shareholders.

The author believes that the above provisions provide a relatively clear basis for minority shareholders of limited liability companies to resolve disputes, dilemmas, and deadlocks regarding company profit distribution through legal channels.

However, in specific application, the above provisions still have issues that need further细化, explanation, and clarification. Among them, how to understand the “effective shareholders’ meeting resolution specifying a specific distribution plan” (hereinafter “distribution resolution”) stipulated in Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law is a controversial and worth-discussing practical issue.

Therefore, the author attempts, through this article, to provide an understanding and analysis of the above issues and the actual application of relevant provisions in China’s judicial practice, as well as the judicial adjudicative rules reflected therein, from a practical perspective. At the same time, suggestions are given for several common problems in the business operation and corporate governance of limited liability companies in practice.

I. Understanding and Application of Distribution Resolutions in Judicial Practice

(I) The Importance of Formal Written Resolutions—Analysis Based on Effective Judgment Documents

Article 15 of Judicial Interpretation (IV) of the Company Law provides that where a shareholder does not submit a shareholders’ meeting resolution specifying a specific distribution plan and requests the company to distribute profits, the people’s court shall dismiss the claim, unless the failure to distribute profits is caused by the abuse of shareholder rights in violation of legal provisions, causing losses to other shareholders. From the perspective of the judicial interpretation’s structure, Article 15 of Judicial Interpretation (IV) of the Company Law corresponds to Article 14 as a “negative” provision, serving as one of the main legal bases for the people’s court to reject a plaintiff’s claim for distribution of limited liability company profits. It can be said that the application of Article 15 of Judicial Interpretation (IV) of the Company Law in judicial practice is an important basis for understanding the above issue and a main avenue for analyzing it.

The author searched the “Wolters Kluwer” legal database for all 82 judgments related to Article 15 of Judicial Interpretation (IV) of the Company Law as of April 24, 2023. After剔除 duplicate cases (second instance, etc.) and cases where the disputed focus was unrelated to profit distribution, 72 documents were最终 obtained as analysis samples (hereinafter “relevant cases”).

Through research on the relevant cases, the author found that: Lawsuits arising from profit distribution have long existed and show a clear increasing trend. Notably, up to 64 judgments (nearly 88%) did not receive court support because the plaintiff shareholder failed to submit a shareholders’ meeting resolution specifying a specific distribution plan. Only in 8 judgment documents did the shareholder/plaintiff’s profit distribution request receive support from the people’s court (hereinafter “supported cases”). The reasons for losing can be specifically divided into three types:

First, the shareholder/plaintiff did not submit any shareholders’ meeting resolution (Situation 1);

Second, the shareholder/plaintiff submitted a shareholders’ meeting resolution, but the resolution content only included agreement to distribute profits without specifying a specific distribution plan (Situation 2);

Third, the shareholder/plaintiff submitted a shareholders’ meeting resolution not to distribute profits (Situation 3).

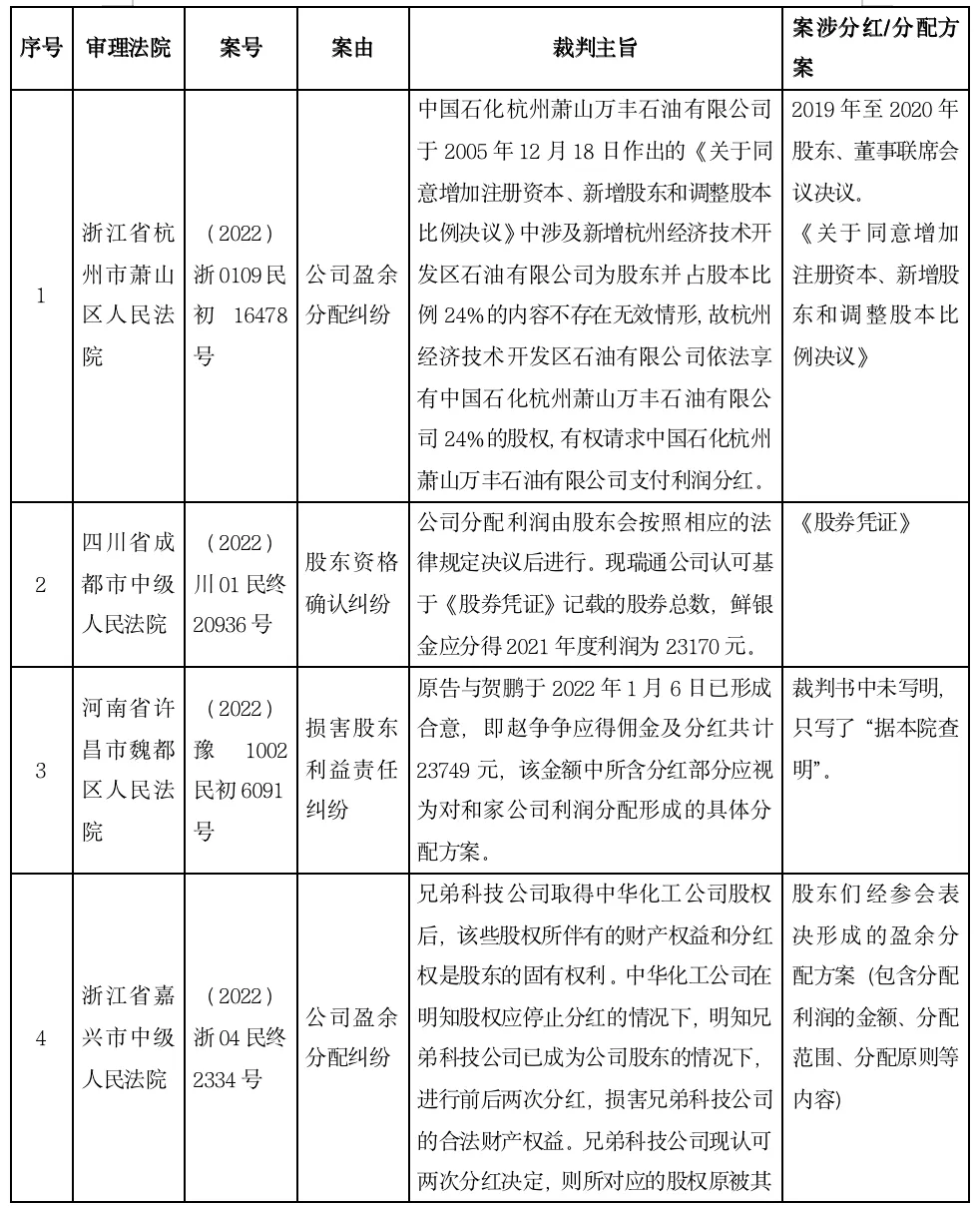

The main circumstances of the above 8 supported cases are as follows:

Analysis of the above supported cases shows a common feature: in all supported cases, the plaintiff/shareholder submitted a complete, written shareholders’ meeting resolution specifying a specific distribution plan, rather than oral agreements or other forms. This reveals the importance of forming and preparing a written, standardized, clear, and specific shareholder dividend plan at the corporate governance level of a limited liability company.

(II) Oral Agreements Carry Significant Legal Risk—The Frustration of Shareholders Behind Typical Negative Cases

Regarding whether oral agreements on limited liability company profit distribution widely existing in practice between shareholders and investors can be supported in judicial practice, the author uses a case from the author’s team’s practice (anonymized) involving a company surplus distribution and shareholder知情权 dispute as a negative example for discussion.

Plaintiff A, as a shareholder of Defendant H Company, sued Defendant H Company, requesting the defendant to pay the plaintiff certain dividends. The reason was that since Defendant H Company sent a “Profit and Profit Distribution Statement” to Plaintiff A on XX date, it had not paid the plaintiff dividends as agreed. At the same time, Plaintiff A submitted audio recordings, claiming that Defendant H Company held a shareholders’ meeting stating it would distribute the remaining net profit before XX month, 202X.

After trial, the court found: Although Plaintiff A was a shareholder of Defendant H Company, according to Article 15 of Judicial Interpretation (IV) of the Company Law, “where a shareholder does not submit a shareholders’ meeting resolution specifying a specific distribution plan and requests the company to distribute profits, the people’s court shall dismiss the claim, unless the failure to distribute profits is caused by the abuse of shareholder rights in violation of legal provisions, causing losses to other shareholders.” In this case, Plaintiff A failed to provide a corresponding shareholders’ meeting or shareholders’ general meeting resolution specifying a distribution plan. The submitted audio recordings could not prove that the company’s shareholders reached an agreement on specific dividends. Therefore, the court ultimately dismissed Plaintiff A’s claim.

Similar cases are not uncommon in China’s judicial practice. Among the more influential ones is the “Henan Thinking Automation Equipment Co., Ltd. v. Hu Ke Profit Distribution Dispute Case”[2]. The Supreme People’s Court held that the plaintiff in this case did not submit a shareholders’ meeting resolution specifying the company’s profit distribution plan; therefore, the claim for ordering the company to distribute profits to the plaintiff lacked a valid legal basis, and the Supreme People’s Court decided not to support it.

It can be seen that oral agreements on profit distribution between shareholders are difficult to recognize as distribution resolutions under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law in judicial practice.

(III) Whether Other Forms of Documents Constitute Distribution Resolutions

In practice, limited liability companies often record and confirm matters related to company profit distribution through forms such as shareholders’ meeting minutes or articles of association. Whether documents of the foregoing forms constitute distribution resolutions under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law is also a practical issue worth discussing.

Although current laws and judicial interpretations do not clearly address this issue, based on relevant judicial practice, it appears that the people’s court tends to recognize that content on profit distribution in the company’s articles of association constitutes a distribution resolution under the aforementioned Judicial Interpretation (IV). For example, in the case “Li Yugang v. Pingdingshan Xianjuyuan Pagoda Cemetery Co., Ltd., Zhang Juping, Zhang Heping, and Yang Yongbing (Company Surplus Distribution Dispute)“[3], the involved company’s articles of association specified a specific profit distribution plan but did not implement it. The plaintiff requested mandatory distribution but was dismissed by the court on the ground that no evidence showed the company had surplus profits. From the adjudicative view of this case, it is not difficult to infer that the people’s court did not deny that the company’s articles of association containing a profit distribution plan could serve as a basis (or one of the bases) for profit distribution.

From the nature of the articles of association, like shareholders’ meeting resolutions, the articles of association of a limited liability company can reflect the unanimous expression of intent by shareholders. By formulating the articles of association, shareholders of a limited liability company stipulate the company’s basic matters and systems, such as organizational structure and corporate governance. It can be said that the process of formulating the articles of association is also a process of reaching consensus among shareholders. Therefore, some scholars believe that the articles of association is an “incomplete open contract.”[4]

Based on the above reasons, the author tends to believe that if the articles of association of a limited liability company specify a detailed profit distribution plan, it may be recognized as (or contain) a distribution resolution under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law.

Furthermore, since limited liability companies in practice often have strong personal relationships and irregular management, in addition to the articles of association, shareholders often use various “meeting minutes” or “meeting documents” (hereinafter “meeting documents”) to clarify certain decisions or changes in the company’s business activities. Can the aforementioned meeting documents constitute distribution resolutions under the above judicial interpretation?

The author believes that the answer to this question should be determined by analyzing the specific circumstances and substantive content of the relevant meeting documents. First, it should be examined whether the executing parties of such meeting documents meet the requirements of a distribution resolution. Specifically, whether the signatories of the meeting documents include the company’s shareholders. If so, it should be further analyzed whether the number and subjects of shareholders who signed and agreed to such meeting documents meet the conditions for effective voting on deciding and approving the company’s profit distribution matters under the Company Law and the company’s articles of association. In other words, if the signatories of the meeting documents are not shareholders of the company (e.g., only the company’s manager, director, or senior management personnel), such meeting documents cannot constitute a distribution resolution under the above judicial interpretation. Secondly, it should be determined whether the procedures for making such meeting documents comply with the procedural provisions on shareholders’ meeting resolutions under the Company Law and the company’s articles of association. Thirdly, it should be considered whether the meeting that produced such meeting documents complies with the rules on shareholders’ meetings under the Company Law and the company’s articles of association. Finally, it should be analyzed whether the content of such meeting documents includes the basic elements constituting a distribution resolution, such as the amount of profit to be distributed and the distribution time. If a limited liability company’s meeting document has one or more deficiencies in the above aspects, it will be difficult for such meeting document to constitute a distribution resolution under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law.

Current relevant judicial practice seems to confirm the author’s above view. Based on the “Wolters Kluwer” legal database, as of April 23, 2023, the author found 37 judgment documents that cited Article 15 of Judicial Interpretation (IV) of the Company Law (2017) and where the plaintiff submitted meeting documents such as meeting minutes as evidence. The author notes that among these 37 judgment documents, the people’s court only responded in writing in 5 of them regarding whether meeting minutes and other meeting documents constituted a specific distribution resolution, and all adjudicative views were negative.

For example, in the case “Wang Jinggang v. Jilin Hualang Environmental Technology Development Co., Ltd., et al. (Company Surplus Distribution Dispute),” the judge explicitly stated: “A specific distribution plan should include specific content such as the amount of profit to be distributed, distribution policy, distribution scope, and distribution time. The attendees of Hualang Company’s April 20, 2018, meeting, except for Wang Bin, were not shareholders of the company. The opinions reached at that meeting were not a shareholders’ resolution. The meeting opinions cited by Wang Jinggang did not specify the amount of profit to be distributed or the distribution time and did not satisfy the constituent elements of a specific profit distribution plan. Therefore, Wang Jinggang’s claim that the ‘Meeting Minutes’ constituted a company dividend document lacks a factual basis and is not supported by this court.”

However, it should also be noted that neither the Company Law nor relevant judicial interpretations have yet denied that meeting documents meeting substantive conditions can constitute distribution resolutions under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law. In relevant judicial practice, when determining that meeting documents do not constitute distribution resolutions, the people’s court mostly focuses on the defects in the substantive content of the involved meeting documents.

Therefore, the author tends to believe that it cannot be simply concluded that all meeting documents cannot constitute distribution resolutions under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law. Meeting documents meeting the substantive requirements also have the possibility of being recognized as (or containing) distribution resolutions. Recognizing that meeting documents meeting the substantive requirements constitute (or contain) distribution resolutions under relevant judicial interpretations is also consistent with the main realities of China’s current commercial practice and business environment.

II. Summary and Recommendations

In conclusion, based on the current main adjudicative views formed by China’s laws and relevant judicial practice, a distribution resolution under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law must simultaneously have the formal requirement of a “written resolution made by the shareholders’ meeting or shareholders’ general meeting” and the substantive requirement of “specifying a specific distribution plan.” It should also be clarified that China’s current laws and judicial interpretations have not provided more detailed explanations of the aforementioned formal and substantive requirements. Therefore, investors, shareholders, and legal practitioners need to carefully assess these issues in practice based on specific circumstances. In this regard, the author, based on relevant judicial practice cases and personal work experience, recommends paying attention to at least the following matters when drafting and preparing a distribution resolution:

-

Whether the distribution resolution is made by the shareholders’ meeting or shareholders’ general meeting, and whether the number of attending shareholders and their corresponding voting situation comply with the relevant provisions of the Company Law and the company’s articles of association;

-

Whether the content of the distribution resolution or the specified distribution rules are specific and clear regarding the distribution amount, time, method (cash or other methods), etc.;

-

Whether the content of the distribution resolution or the specified distribution rules comply with laws and the company’s articles of association, whether they contravene the characteristics or essence of equity investment, and whether they contravene accounting standards or accounting principles.

At the same time, in business operation and corporate governance, “bosses” should have a basic understanding of “written documentation.” Based on current laws and relevant judicial practice, oral agreements are difficult for the people’s court to recognize as distribution resolutions under Articles 14 and 15 of Judicial Interpretation (IV) of the Company Law. “Bosses” should avoid failing to document profit distribution and related agreements in written legal documents due to trust or negligence, which may ultimately lead to the legal risk of their investment becoming “money down the drain.”

Notes:

[1] In capital market transactions, generally speaking, the vast majority of equity and securities investors (both primary and secondary) do not pursue dividends from the equity or shares (i.e., capital) they hold. Their means of realizing returns is to trade the capital itself through various forms (such as initial public offering (IPO)—capital exit).

[2] See the Supreme People’s Court (2006) Min Er Zhong Zi No. 110 “Henan Thinking Automation Equipment Co., Ltd. v. Hu Ke Company Surplus Distribution Dispute Second Instance Civil Ruling.”

[3] See the Henan Provincial High People’s Court (2018) Yu Min Shen No. 6223 “Li Yugang, Pingdingshan Xianjuyuan Pagoda Cemetery Co., Ltd. Company Surplus Distribution Dispute Retrial Review and Trial Supervision Civil Ruling.”

[4] Luo Peixin, “Contractual Interpretation of Company Law,” Peking University Press, 2004, p. 142.