Five Dimensions to Consider When Building an Equity Structure

Five Dimensions to Consider When Building an Equity Structure

The design of an equity holding structure should revolve around the specific purposes of the shareholders. This article systematically explains the advantages and applications of different shareholding models from five core dimensions: first, establishing a limited liability company as a holding platform to effectively isolate project company debt risks; second, using a holding platform to optimize dividend and share reduction tax burdens and facilitate reinvestment; third, in mergers and acquisitions, utilizing a holding company to qualify for special tax treatment and achieve deferred taxation; fourth, leveraging a holding company to coordinate financing guarantees, asset承接, and business incubation to enable capital operations; and fifth, in family wealth inheritance, using a holding company to retain earnings and avoid dividend individual income tax to target support for the next generation's entrepreneurship. Enterprises should flexibly combine these dimensions based on actual strategic needs to build the optimal equity structure.

#1

Previously, the author published a series of articles on the “Longan Guangzhou Law Firm” WeChat public account (click the blue text to view: Equity Partnership, Private Enterprise Equity Inheritance), which discussed equity distribution and equity partnership mechanisms. After equity distribution is completed, in what form should shareholders hold the company’s equity? Before discussing this question, the author provides an example.

Case: A project company has two shareholders, Founder A and Founder B. Shareholder A has a 70% equity ratio, and Shareholder B has a 30% equity ratio. So, for Shareholder A’s equity, what holding structure is more reasonable?

The author believes that the holding structure depends on the purpose that Shareholder A wants to achieve. Different purposes lead to different holding structures. The author elaborates from the following five dimensions.

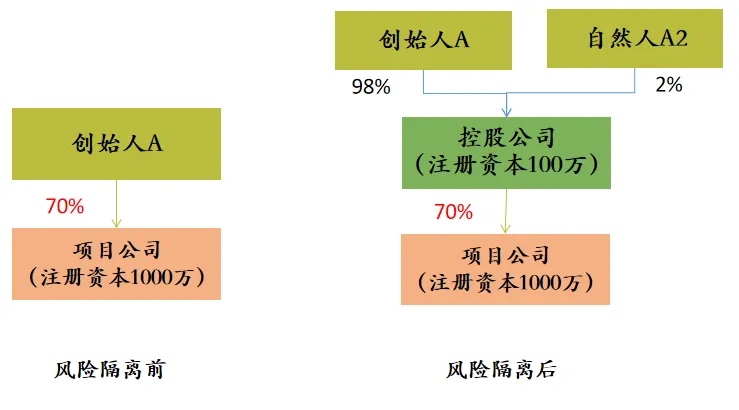

(A) Debt Risk Isolation Dimension

To prevent the project company’s debt risks from being transmitted to Shareholder A, the characteristic of limited liability companies—“shareholders bear limited liability to the extent of their subscribed capital”—can be used. A can establish a limited liability company as a holding platform, which then holds the equity of the project company.

The equity structure is shown in the following diagram:

Note:

-

The reason A and B jointly establish the holding company is that if the holding company is a single-shareholder company, according to the Company Law, A would bear joint liability for the holding company’s debts unless A proves that there is no financial混同 between A and the holding company.

-

Subject B should try not to be in a marital relationship or直系亲属 relationship with A, as this could easily be deemed by judicial authorities as实质上 a single-person company.

-

Since shareholders bear limited liability within the scope of subscribed capital, the registered capital of the holding company does not need to be too high.

Legal Basis:

Article 63 of the Company Law: Where a shareholder of a single-person limited liability company cannot prove that the company’s property is independent from the shareholder’s own property, the shareholder shall bear joint liability for the company’s debts.

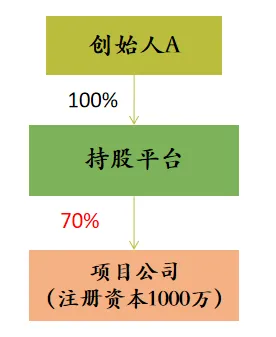

(B) Tax Optimization Dimension

From a tax optimization perspective, a holding platform is generally established (which can be registered in certain tax-favorable areas). The大致 structure is as follows:

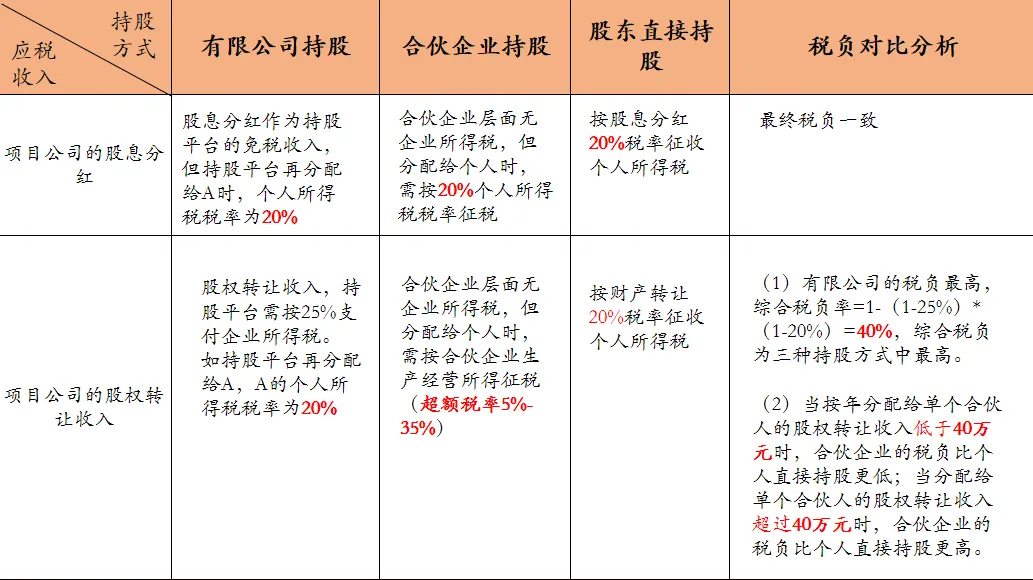

Tax Analysis Comparison:

Q1

Since the tax burden of a holding platform has no advantage over direct shareholding by natural persons, why consider using a holding platform?

A1

(1) When the project company’s dividend is distributed to the holding platform (limited company), as long as the holding platform does not distribute to A, no individual income tax arises.

(2) If the holding platform (limited company) uses the proceeds to invest in other industries, the holding platform (limited company) can serve as a capital operation platform for horizontal expansion into other industries, and the holding platform (limited company) has significant tax planning space.

(3) For a holding platform (partnership), as long as the partnership has profits, regardless of whether they are distributed to partners, the partners are subject to individual income tax. A partnership form of holding platform is generally suitable for employee shareholding platforms.

Q2

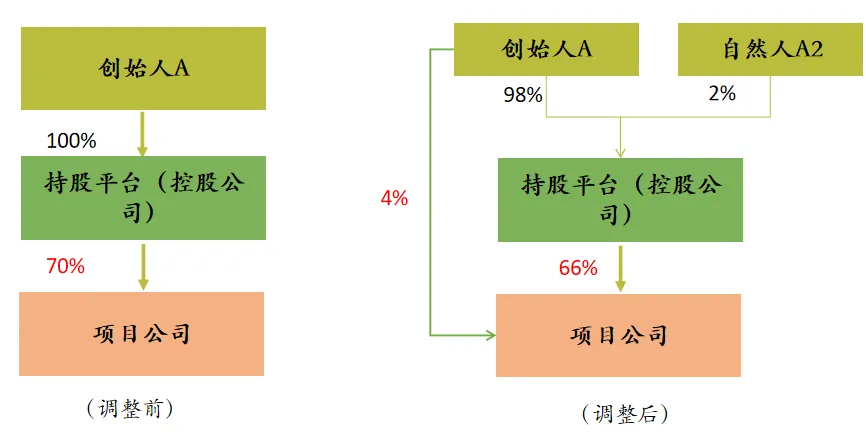

If the project company goes public and Shareholder A wants to reduce some shares for personal family asset allocation, how should the equity structure be designed?

A2

As mentioned above, the comprehensive tax rate for Shareholder A’s share reduction income through the holding platform (limited company) is 1-(1-25%)*(1-20%)=40%. Therefore, if the company has listing plans and the actual controller needs to reduce some shares for personal life needs, a combination approach can be adopted where the actual controller directly holds a small portion of shares, with the remaining majority held through a holding platform.

For example, the following shareholding method can be adopted:

Explanation:

-

When the company’s shares are listed, the controlling shareholder generally needs to undertake not to reduce shares within 3 years. Moreover, to maintain the stability of the company’s stock market value, large-scale reduction by controlling shareholders is relatively rare.

-

Under the above equity structure, Founder A directly holds a small portion of the listed entity’s shares (recommended 1%-5%). If Founder A needs to cash out, they can do so from this portion. At this point, the tax rate on Founder A’s cash-out income is 20%, which is much lower than cashing out through the holding company.

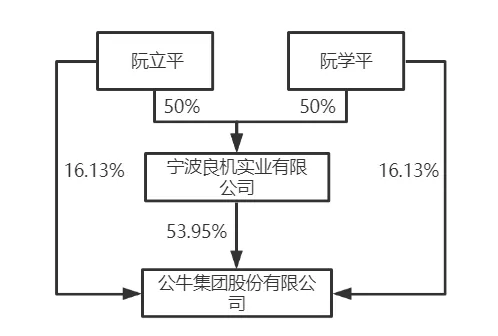

In a real case, Bull Electric adopted the above structure:

(C) Merger and Acquisition Dimension

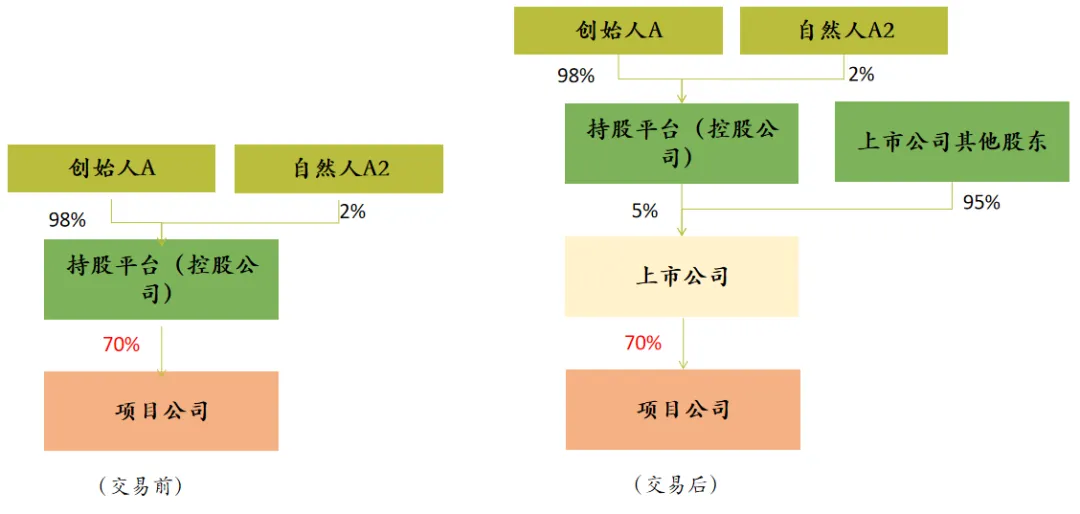

Assume that A holds 70% of the project company’s equity through a holding company, with a book value of RMB 7 million. A listed company plans to acquire the 70% equity held by the holding company in the project company by issuing additional shares (the fair value of this equity is RMB 200 million). After the transaction, the holding company holds 5% of the listed company’s shares (as shown in the diagram below).

According to Caishui [2009] No. 59, Caishui [2014] No. 109, and Caishui [2014] No. 116, the holding company may elect to apply special tax treatment in the above transaction, meaning that the holding company does not need to recognize equity transfer income at fair value at the time of the transaction.

In the above case, if Shareholder A directly held 70% of the project company’s equity, the above transaction would not qualify for special tax treatment (but could recognize the taxable income from the equity transfer over 5 years under Caishui [2014] No. 116). Therefore, from the perspective of M&A tax policy, holding equity through a holding company is more advantageous than direct personal shareholding.

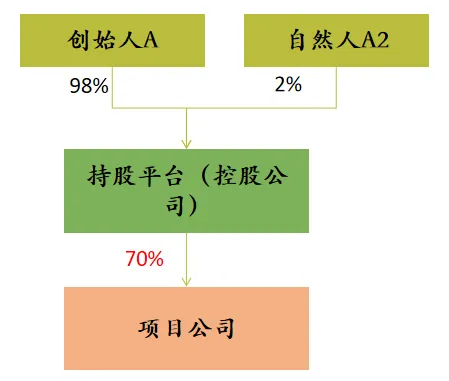

(D) Capital Operations Dimension

From the perspective of capital operations, Founder A generally needs to establish a holding company to hold the project company’s equity, rather than directly holding shares as a natural person. The equity structure is generally as follows:

The above shareholding structure serves the following purposes:

-

The holding company can provide guarantees for the debt financing of the listed company (or company planning to list), improving the credit rating of the listed company’s debt and reducing financing costs.

-

The holding company can be ready at any time to take over non-quality assets from the listed company, coordinating resources for the listed company’s future development.

-

Establish a holding company to hold businesses in the listed entity that are not yet suitable for listing or are not yet mature. When the time is right, these can be listed separately (domestically or internationally, on A-shares or the New Third Board) or injected into the listed company through a private placement.

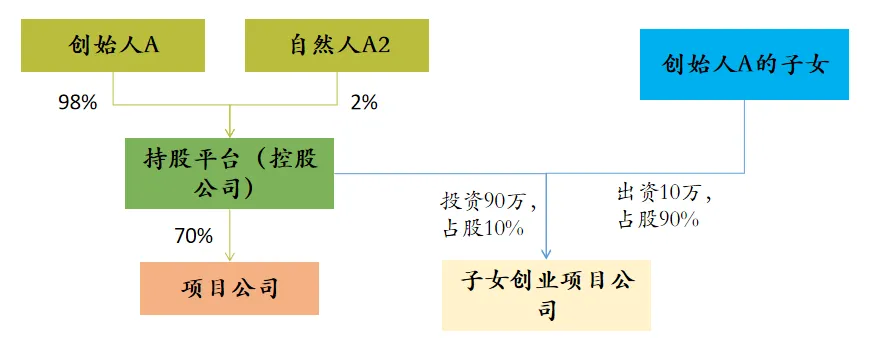

(E) Wealth Inheritance Dimension

If A’s children wish to start their own businesses outside A’s company system, the holding company can jointly invest with the children to establish a project company, with the holding company holding a minority stake and the children holding a majority stake. However, the holding company contributes most of the capital, while the children contribute only a small portion.

Through this method, the dividends and proceeds from share reduction obtained by the holding company from the project company do not need to be first distributed to A and then used by A to support the children’s entrepreneurship. This avoids the individual income tax that would arise from distributing the holding company’s profits to A.

The equity structure is as follows:

Zhang Jing

Senior Partner of Beijing Longan (Guangzhou) Law Firm

Emerging Talent in Guangdong Foreign-Related Lawyers

Zhang Jing has long practiced in the fields of equity structure design, corporate M&A and restructuring, cross-border investment and financing, private equity funds, and equity incentives.